Markets in the Fog of War

Crisis narratives that form, spread, and mislead investors

Overview

After 12 days of bombing in the Middle East, markets are still operating in the fog of war. These times can be disorienting, and in that confusion it’s easy to latch onto the loudest, simplest explanations. But these narratives can be misleading.

In this piece, we’ll examine some of the stories currently circulating in markets and why they can feel convincing in moments like this. We’ll suggest that the real opportunity lies in stepping beyond the fog and looking for the dynamics that aren’t being widely discussed as clarity slowly returns.

Setting the Scene

The conflict has been polarising for markets and participants alike. Commentators are making drastic calls about the impact to the economy and the outlook for stocks:

The recessionistas are calling for an imminent downturn. AI is displacing white-collar jobs. Oil supply is being choked in the Strait of Hormuz, pushing energy prices higher and squeezing consumers and businesses alike. Layer on housing at all-time highs relative to incomes and historically weak household borrowing, and the result, they say, is straightforward: rising costs, weakening demand, and a recession.

The inflationistas agree oil prices could rise, but they see structural forces keeping the economy afloat. G7 rearmament, supply chain reshuffling, and a massive buildout of data centers and power infrastructure are all driving sustained demand for labor, capital, and energy. Higher prices, in their view, don’t tip the economy into recession, they just keep inflation elevated while growth carries on.

In uncertain times, people default to binary outcomes. But that’s not how markets work. The reality is complex, and that complexity creates opportunities.

Narratives

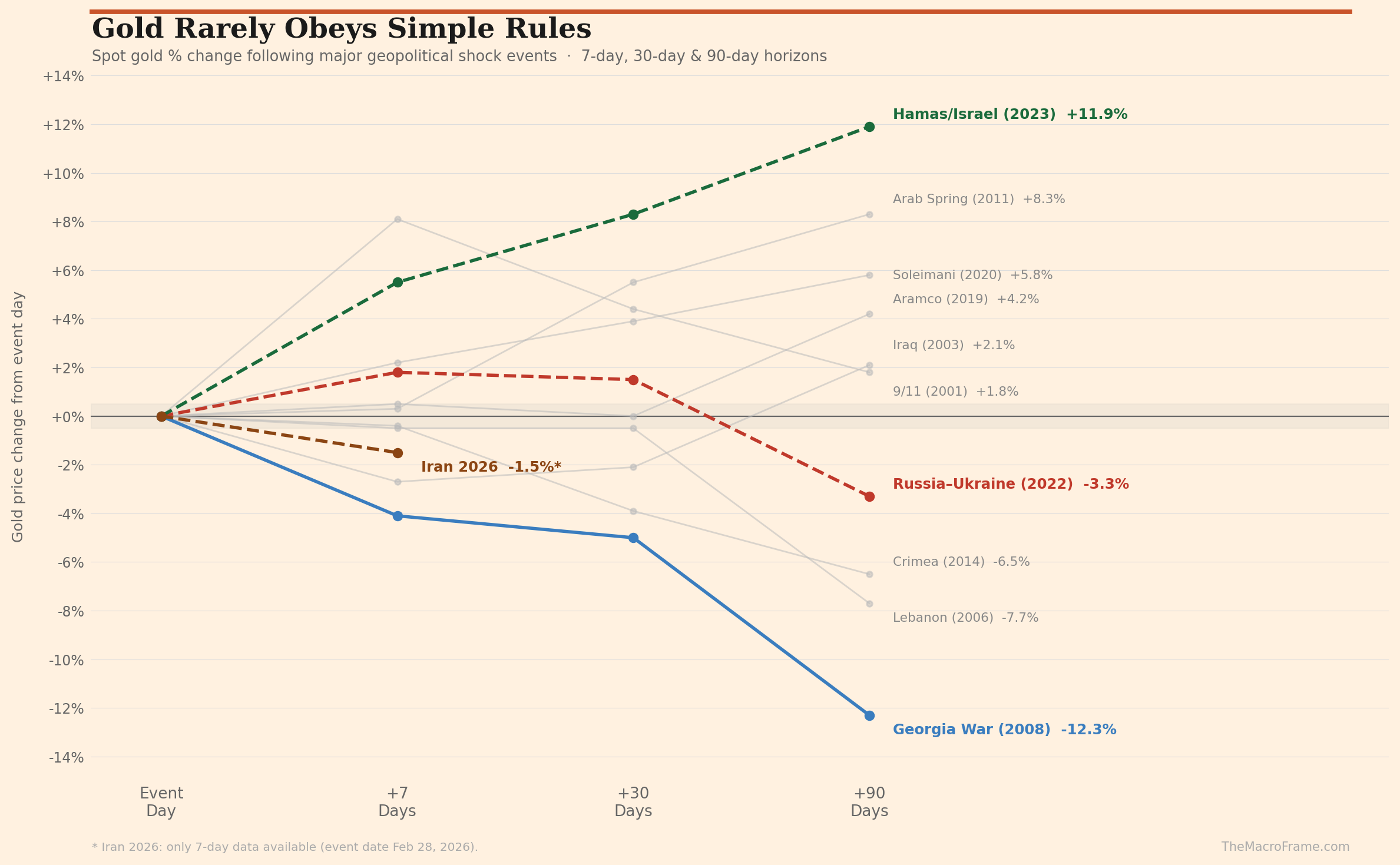

“Gold always rises during major geopolitical shocks.”

It fascinates me how people adopt simple rules for complex events.

Over time, these rules become accepted wisdom. If X happens, then Y must follow. One common example is the belief that gold always rises during geopolitical shocks.

It makes sense. War creates uncertainty, uncertainty drives investors toward safe havens, and gold is one of the oldest safe-haven assets.

But it’s not true.

Sometimes gold rises during geopolitical shocks. At other times it barely reacts, or declines.

Take the current Iran 2026 conflict. Gold spiked slightly on the day of the event, but was down 1.5% over the following seven days.

Context matters. Gold had already risen 25% in 2026 before the conflict began. The move had already occurred before the narrative arrived.

Think of markets like a chess game where the rules are always changing and you need to be three or four moves ahead. By the time a narrative reaches consensus, it’s too late. Then the rules change.

Here’s a quick illustration. A market participant calls for gold to spike on geopolitical risk. Another responds sarcastically: “so brave.” When a trade becomes obvious enough to be mocked, the move may already be exhausted.

Three lessons follow.

Simple market rules are rarely reliable: if a relationship sounds obvious, it may already be priced in.

Context matters: if a large move has already taken place, weakness once the narrative becomes obvious can signal exhaustion.

The best trades emerge before consensus forms: by the time a narrative feels widely accepted, the opportunity has usually been rinsed.

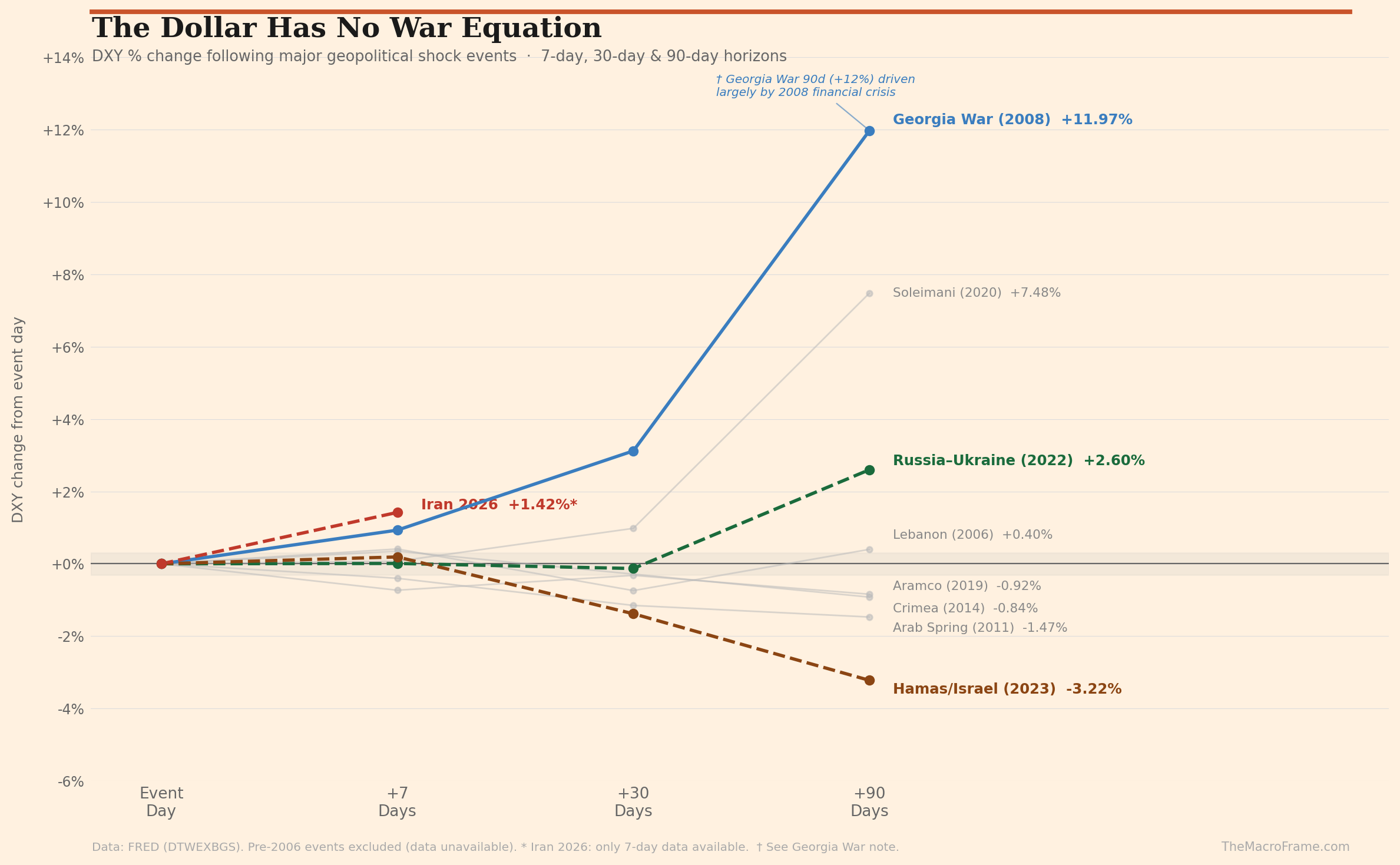

“The USD goes up when conflict occurs.”

The USD is also seen as a safe haven during conflicts. The DXY did rise after the US-Israel-Iran conflict began, and it also rose after the Russia-Ukraine war.

But that’s not the rule.

The USD is not governed by war. It moves relative to other currencies based on countless factors.

The current shock highlights a deeper complication: markets can anticipate events.

There were already signs of a USD uptrend at the start of 2026, two months before the conflict began.

Which came first, the price move or the explanation for it?

Some will argue that the dollar strengthened because markets anticipated the conflict. Others will say the dollar was already set to rise for entirely different reasons, and the war narrative simply arrived afterwards. The truth contains elements of both. By the time an event is newsworthy, prices have often already moved.

At The Macro Frame, we turned bullish on the USD in February 2026 for reasons that had nothing to do with war. Our view was based on market psychology and technical signals developing in gold markets, patterns that have appeared repeatedly over decades.

This highlights another lesson: major market moves rarely come from a single cause. They emerge from confluence. Market psychology, technical structure, fundamental pressures, and the news cycle often align at the same time. When multiple forces point in the same direction, the probability of a move increases. Miss one signal and the outcome may still be the same.

That is why our framework combines psychology, fundamental analysis, and technical analysis. When those forces align, we act.

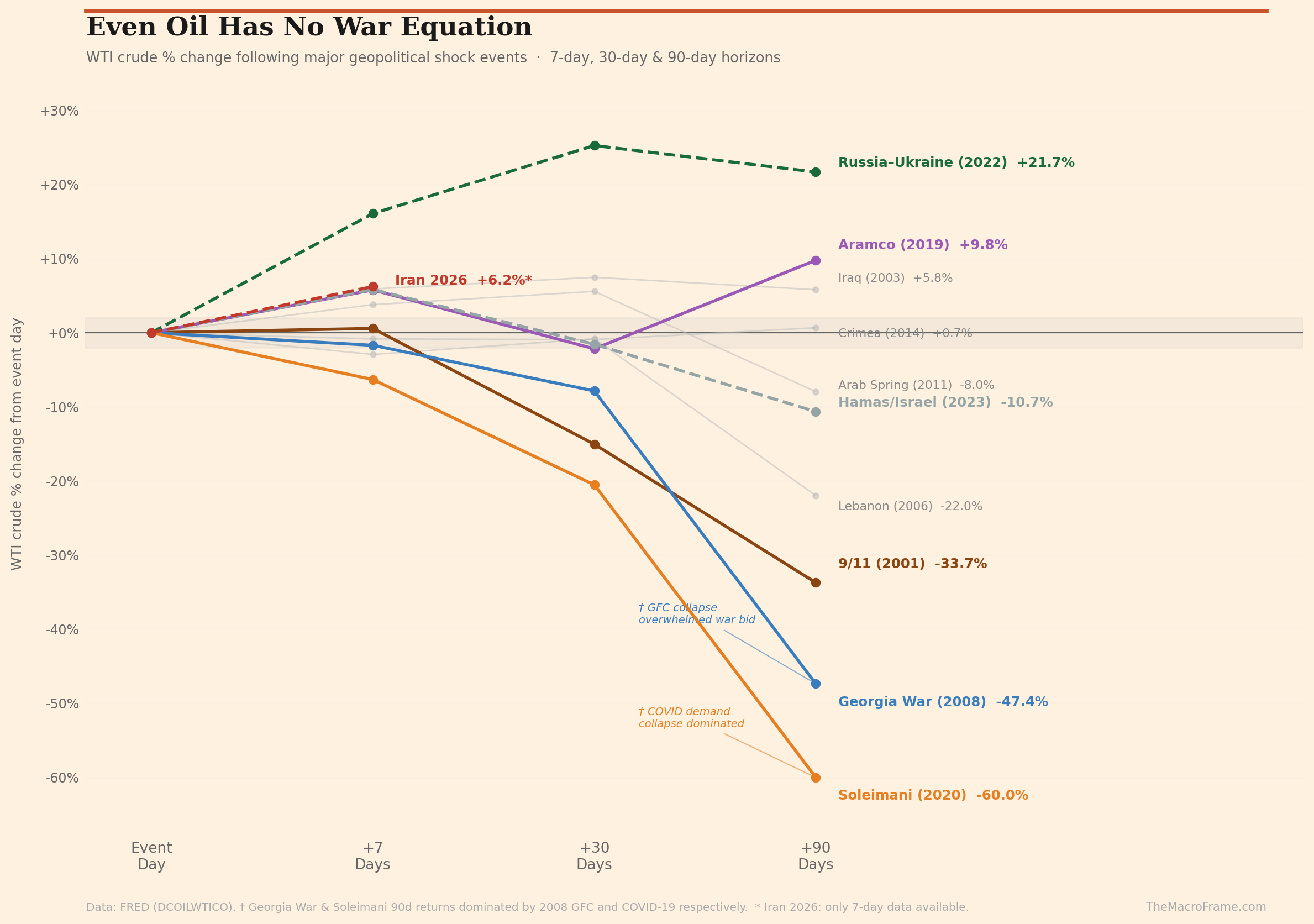

“Oil went up, so oil companies like Exxon will go up.”

Sometimes markets do have clearer mechanics.

Oil has more transparent supply and demand dynamics than the USD. Around 20% of global oil passes through the Strait of Hormuz, so disruptions there have a meaningful impact on supply. Oil prices had not surged dramatically in 2026 before the conflict, which meant there was room to move higher once geopolitical risk increased.

But look at the data across eleven conflicts since 2001. Oil has risen in some cases and fallen in others, depending on the specific dynamics of each event. The Aramco attack, which was the largest single-day oil spike in history, had fully retraced within a month.

Traders were correct that oil would rise for the Iran 2026 conflict. However, many also assumed oil equities would rise alongside it. That is not the same thing.

Crude oil reflects the price of a physical commodity today. Oil equities represent businesses valued on years of future production. Front-month oil can surge while oil stocks remain muted or decline.

This is where many pundits got the trade wrong. Their view on oil was correct, but their instrument was not.

An oil company is not a barrel of oil. It is a business with years of future production, capital costs, and broader sector exposure. Identifying the right trade is only half the job. The other half is choosing the right instrument to express it.

Hidden Dynamics

We’re 12 days into the conflict and it remains unclear how or when it will end.

But this much is becoming clearer: this is the opening move in a decade-long war for energy security. Access to reliable, affordable energy is the defining constraint of the next decade. This conflict just made that visible.

In the short term, attention remains locked on the loudest signals: gold, oil, the dollar. But within the energy complex itself, the more interesting story is playing out in quieter corners.

Natural Gas: The Catch-Up

Oil has dominated the headlines, but natural gas has received less attention. Yet it may be where the more acute supply shock is playing out. Qatar has declared force majeure on roughly 25% of global LNG supply, sending European gas prices sharply higher. US Henry Hub has followed, albeit more modestly.

Retail attention remains locked on crude while the LNG story plays out more quietly. This is exactly the kind of divergence that tends to close eventually, and quickly.

The fundamentals reinforce it. Natural gas is unavoidable for grid stability, industrial production, and powering the data center buildout behind AI. Nuclear is the likely long-term answer, but new capacity is a decade away. For now, gas fills the gap.

Coal: The Fuel Nobody Wants to Talk About

Taiwan has 11 days of natural gas reserves. All of it comes from Qatar. With force majeure declared on roughly 25% of global LNG supply, Taiwan is already diverting orders to Australian and Indonesian coal. South Korea and Japan are not far behind. Europe, facing the same gas squeeze, is turning to South African and Polish coal.

The political calculus is straightforward. Between the pollution 20 years from now and no electricity today, every politician makes the same choice.

This is the fuel-switching mechanism playing out in real time. When Henry Hub rises and LNG tightens, coal doesn’t disappear — it comes back. The seaborne thermal coal market, which most investors have written off entirely, is now the marginal supplier to some of the world’s largest economies.

Indonesian, Australian, and South African producers are the direct beneficiaries. They were unloved before this conflict began. That’s precisely why the move, when it comes, tends to be fast.

Examples

Australian: Whitehaven Coal (WHC.AX), New Hope (NHC.AX), Yancoal (YAL.AX)

Indonesian: Adaro Energy (ADRO.JK), Bukit Asam (PTBA.JK)

South African: Thungela Resources (TGA.L / TGA.JSE)

Conclusion

The narratives forming right now feel urgent and convincing. They always do in the fog of war.

But as we’ve seen with gold, the dollar, and oil, the rules that feel most reliable during a crisis are often the ones with little historical support.

By the time a narrative reaches consensus, the trade is usually crowded, late, or already over. The edge lies in identifying what comes next before the crowd does, and having the discipline to exit once it becomes obvious.

The real questions are second-order. Not “will oil rise?” but “which instrument captures that correctly?” Not “will the dollar surge?” but “was it already moving before anyone had a reason to explain it?”

Complexity is uncomfortable. But it is also where the edge lives.

The fog will lift. It always does. The question is whether you were thinking clearly while everyone else was following the noise.