PayPal: Investor Pain Becomes Opportunity

A Contrarian Setup in Plain Sight

The Contrarian Setup

PayPal (PYPL 0.00%↑) is now one of the most hated large-cap fintech stocks.

Growth has slowed, competition has increased, and the stock has lost most of its initial gains. Many investors now see it as a stagnant payments platform.

Consensus predicts decline and ongoing irrelevance as competitors gain market share. Yet, the core business is still profitable, cash-generating, and integral to global commerce.

The Thesis

PayPal offers asymmetric risk/reward at current prices because:

Sentiment has shifted from excitement to frustration.

The business is still profitable despite slower growth.

Valuation suggests decline instead of stability.

Technical indicators show long-term support is forming.

Sentiment

I remember using PayPal in the early 2000s. They locked my account and asked for a fax of my life story to unlock my funds. As an eBay seller, this was incredibly frustrating.

Fast forward 25 years and that same frustration is reflected in sentiment around the company today.

It remains widely known that PayPal can freeze accounts or hold funds unexpectedly. Some things never change.

Investor frustration is now just as visible. In many circles PayPal has become synonymous with disappointment, often jokingly referred to as “PainPal”.

Contrast

Back in the early 2000s, PayPal was a favorite of the internet boom.

After spinning off from eBay in 2015, sentiment was very positive. Investors viewed it as a top digital payments platform worldwide and a top growth stock.

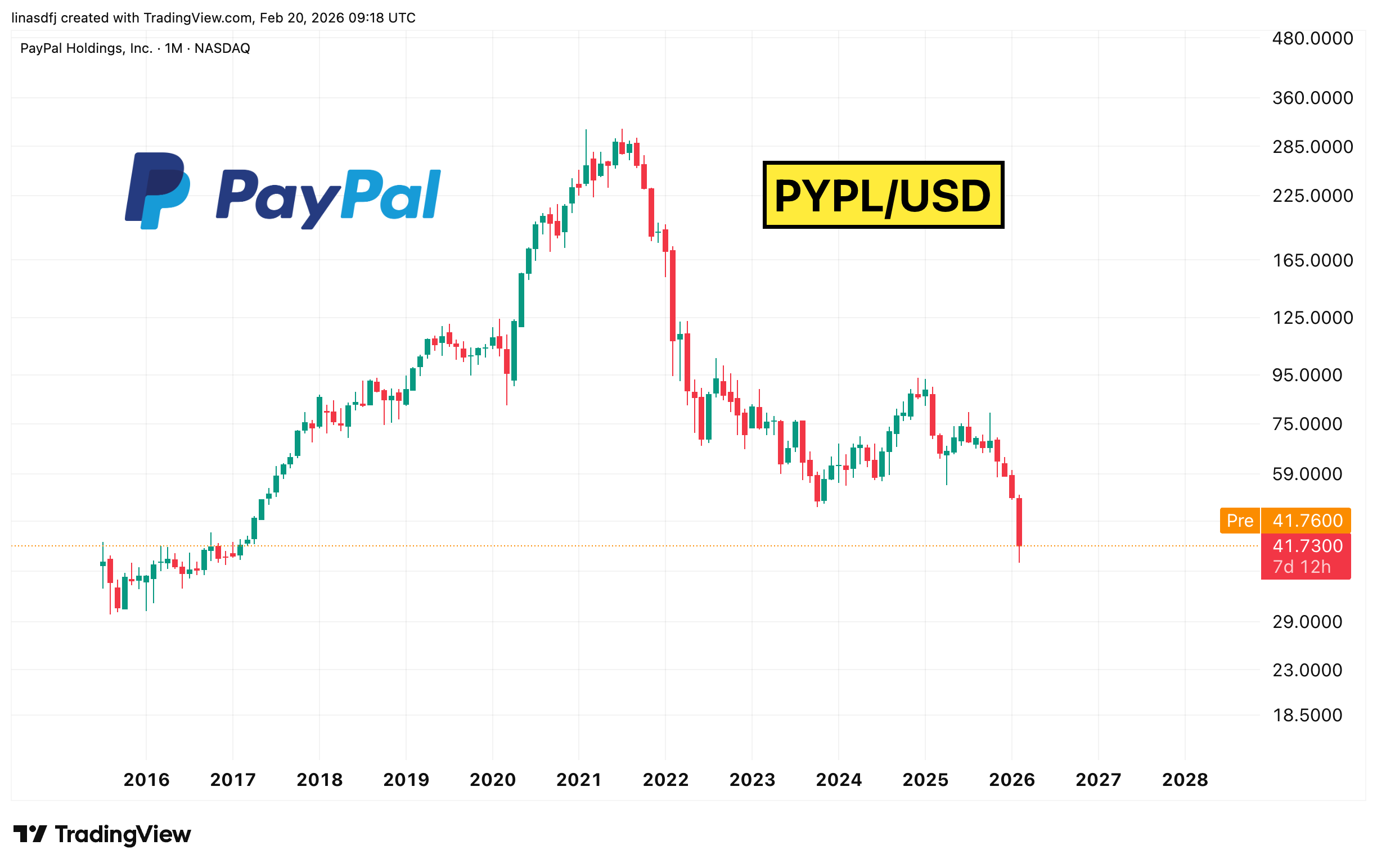

Over the next six years, the stock rose about tenfold, from around $28 at relisting to nearly $300 at its 2021 peak. It became a core growth holding during the zero-rate era.

Then growth stalled. After 2021, the stock gave back almost all those gains. Today, PayPal trades not far above its initial valuation as an independent company.

To show how weak this performance has been, let’s compare PayPal to the Nasdaq.

Comparing PayPal to its index helps us see its performance over time against similar companies.

Exhaustion

Sentiment is now so weak that even traditional value-investing communities show little interest. Comments include:

“It’s a sinking ship.”

“I wouldn’t buy it even for 20.”

“… closer to a speculative gamble.”

Even among those still holding shares, the tone reflects fatigue:

“Bag holder… big buybacks yet to have an effect.”

“Fed up watching the money bleed.”

My rough indicator is simple: when broad investing communities are bearish, I put a stock on my watchlist. When even value-oriented investors show little interest, it deserves deeper analysis.

Technical Analysis

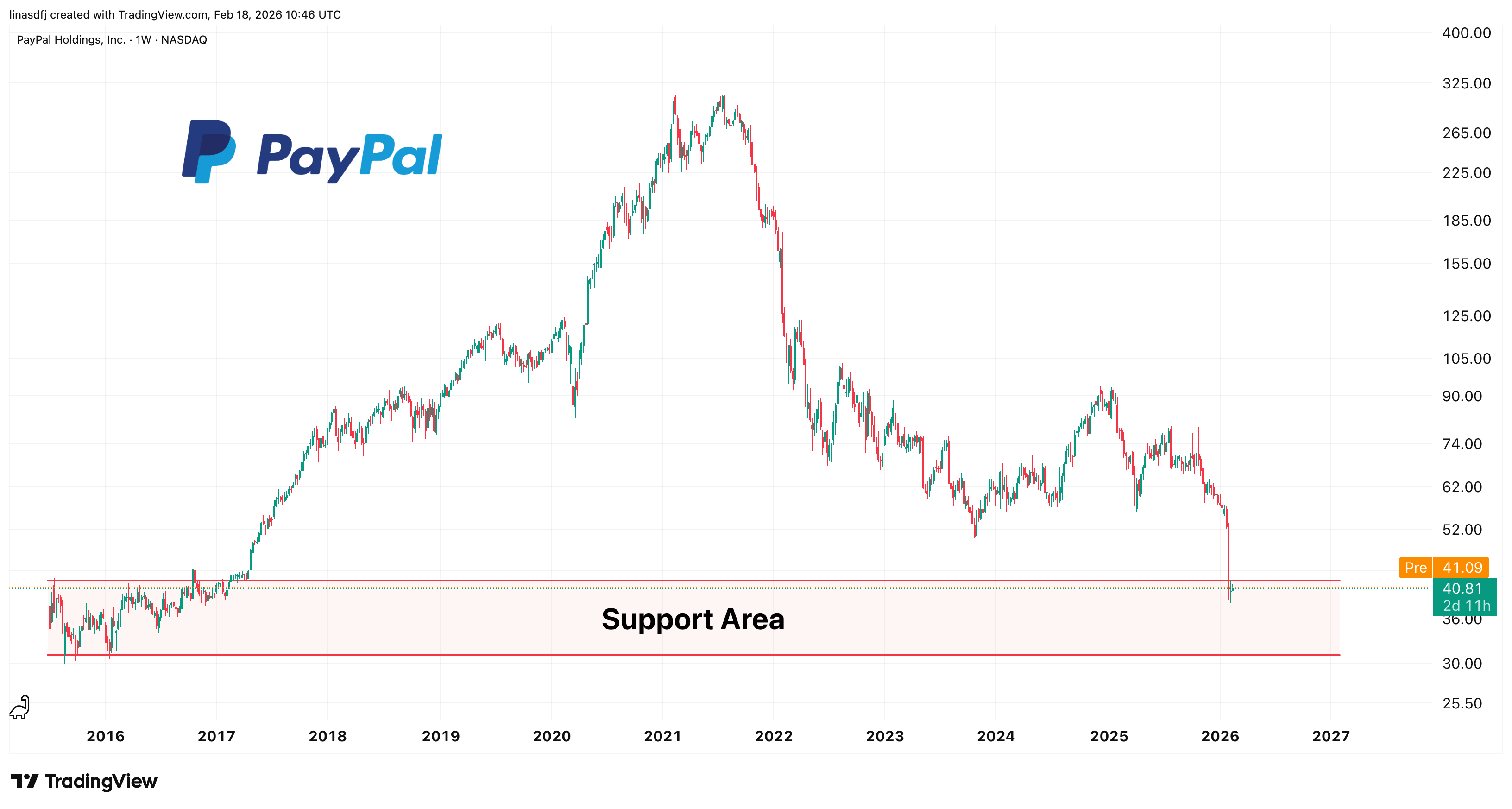

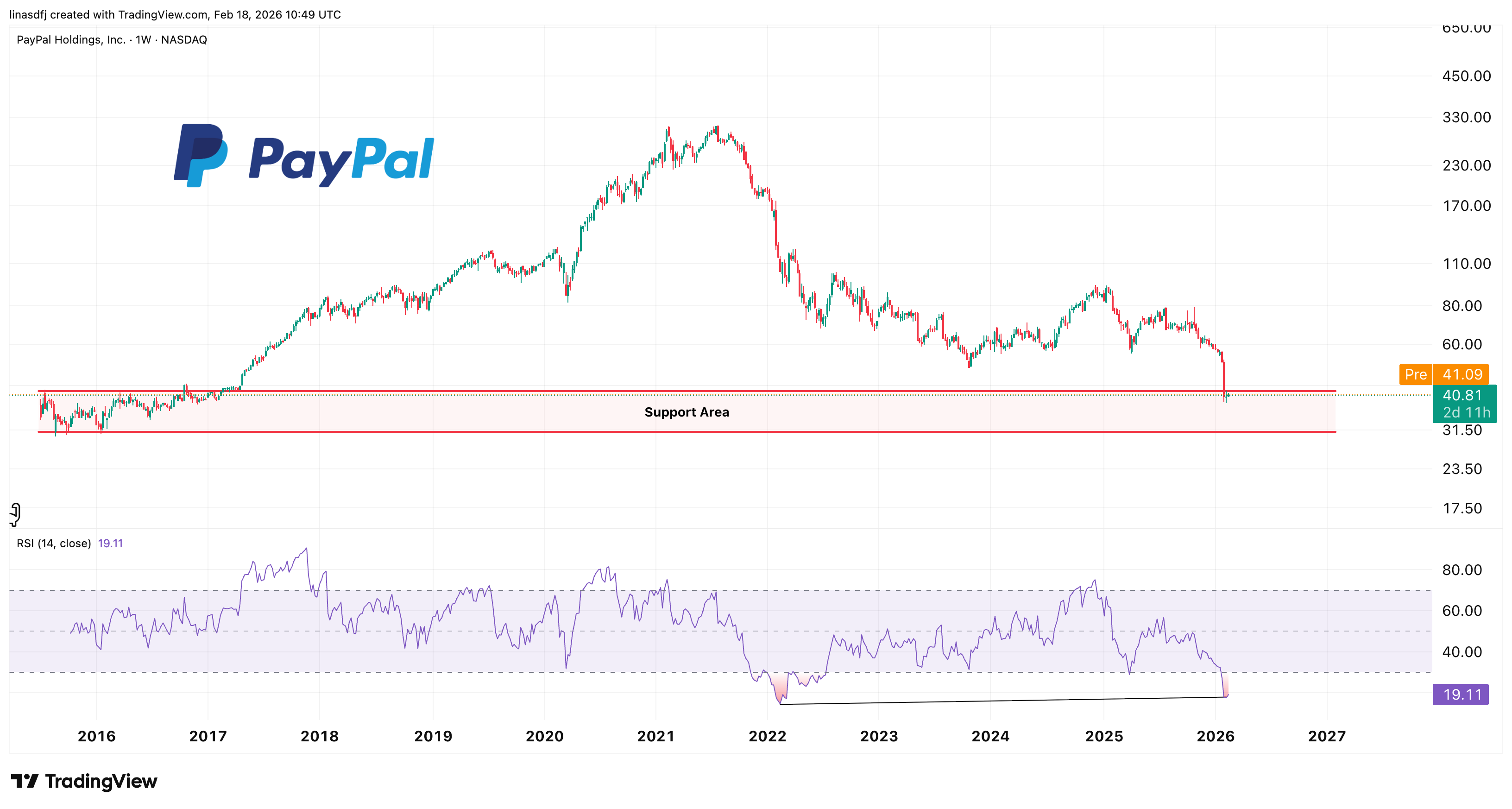

The stock is now trading back toward its initial valuations from 2015, providing major long-term support.

There’s bullish divergence forming on the RSI, suggesting that downward momentum is weakening as the price revisits lows.

Bullish RSI divergence often signals potential entry points during oversold conditions, especially when RSI drops below 30 and begins to rise.

Fundamentals

Despite negative sentiment, the business remains strong.

PayPal’s network is deeply embedded. It serves hundreds of millions of accounts and tens of millions of merchants globally. For many businesses, switching payment providers can be risky and complex, creating significant switching costs.

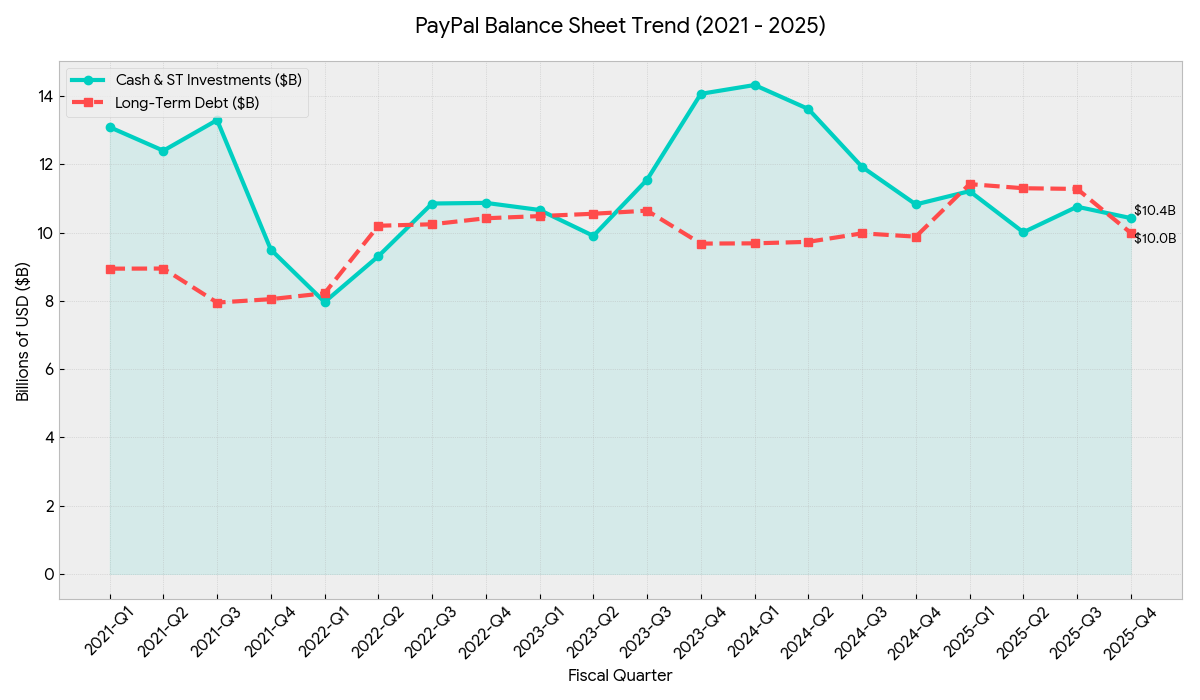

The balance sheet is healthy, with cash roughly equal to debt and solid free cash flow.

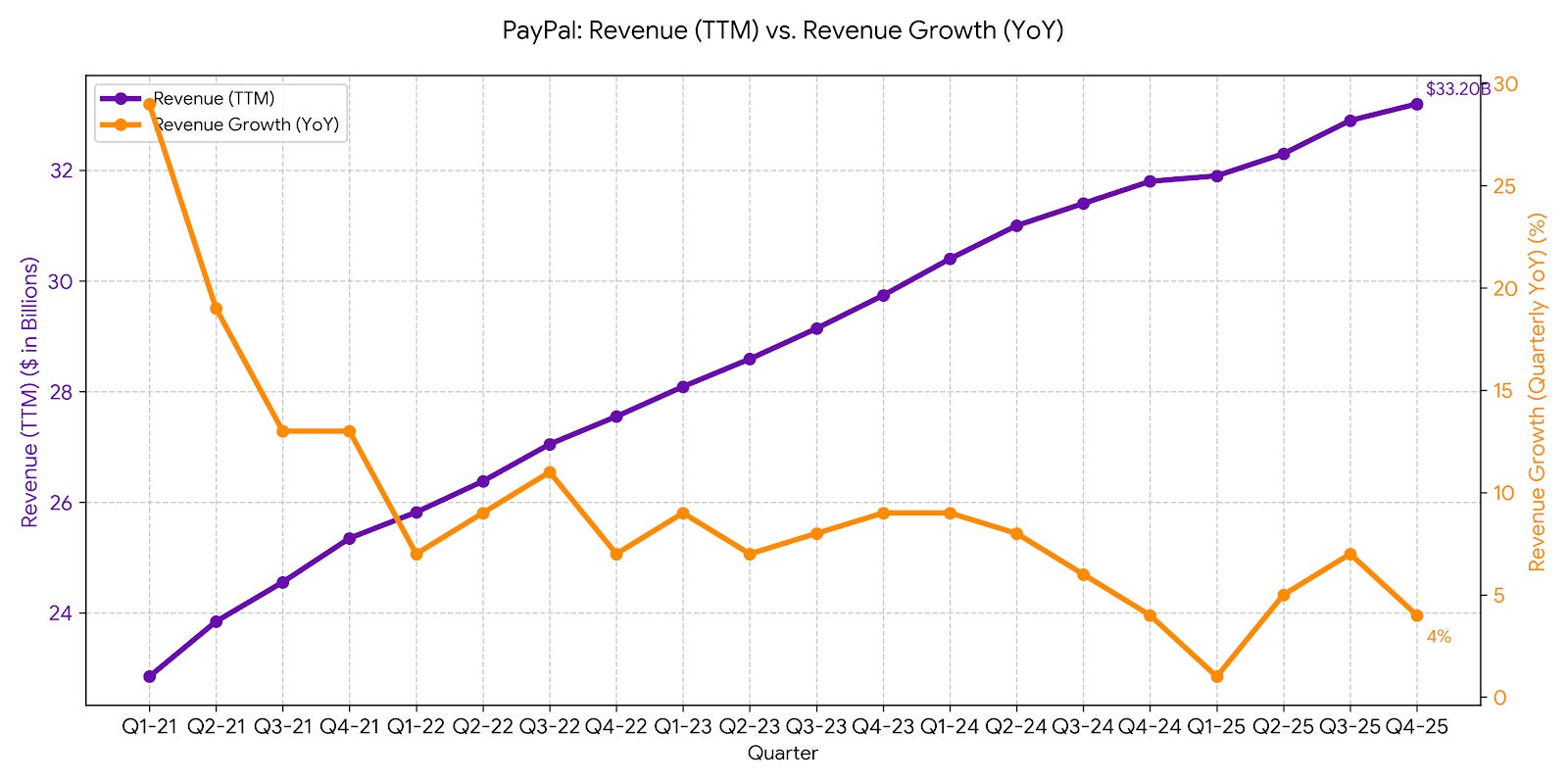

The issue is growth. Revenue expansion has slowed significantly since its high-growth years.

Part of this slowdown is strategic; management is intentionally pivoting away from low-margin volume in favor of higher-quality revenue and operational efficiency.

Valuation

PayPal now trades at about 7–8x forward earnings and under 5x EV/EBITDA, making it one of the cheapest large-cap fintech and payments companies globally.

Despite the low valuation, profitability is strong. Return on equity is around 20–25%, and return on assets is about 4–5%, both healthy for a global payments platform.

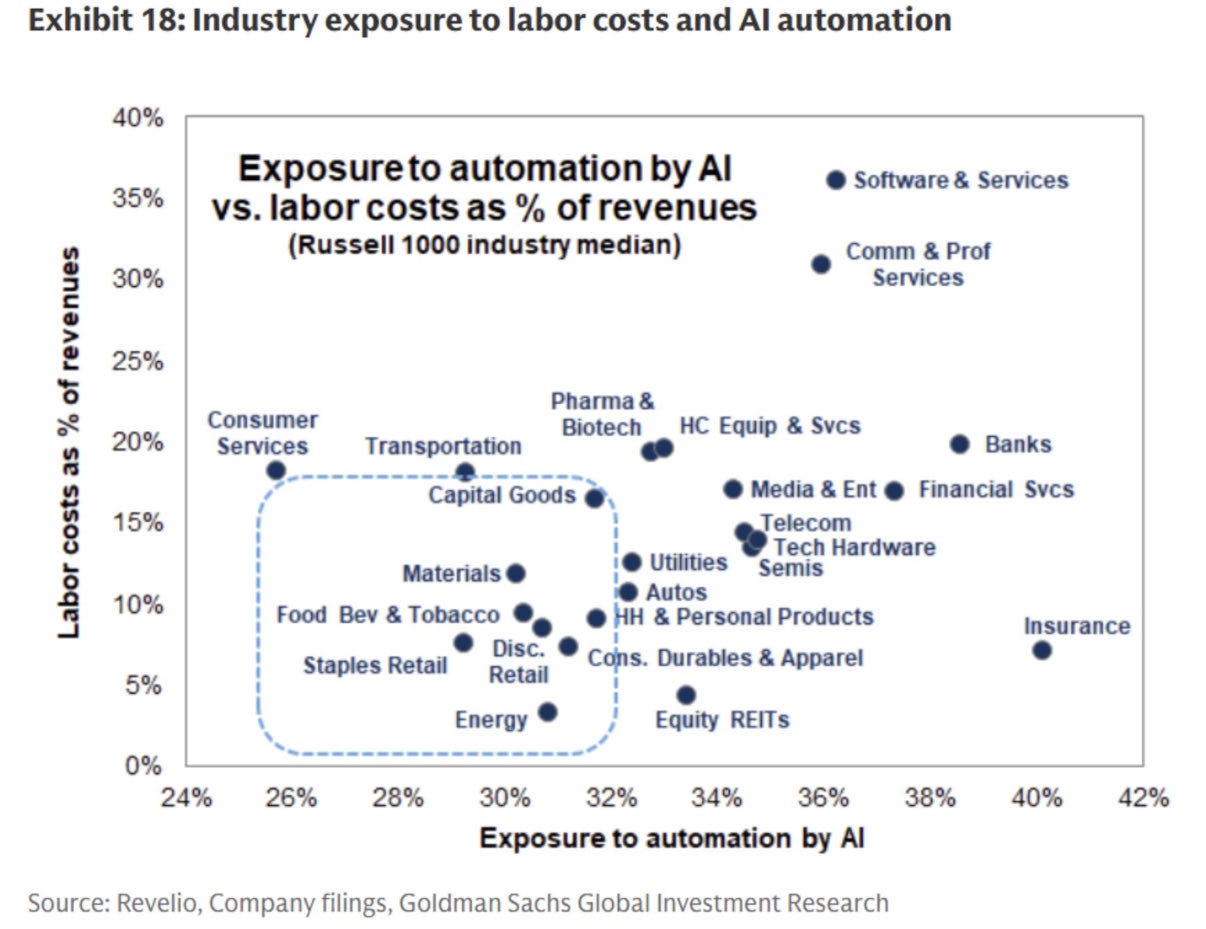

AI disruption

There’s a narrative that AI will hurt software and fintech margins through competition. This may be true for some firms. However, for financial infrastructure companies with a strong moat, the opposite might happen.

Banks, insurers, and payment networks face high back-office labor costs. Areas like compliance and fraud detection are being rapidly automated by AI. As these processes become more efficient, costs drop while transaction volumes grow.

Dividends

PayPal recently introduced its first dividend, with an initial yield of about 1–2%. This marks a shift toward a more mature capital return profile.

Even a modest payout can help reposition the company as a value stock, attracting investors focused on yield rather than just growth.

Share Repurchases

Management plans to buy back ~$6B in shares in FY2026. At current valuations, these buybacks will retire enough stock to increase each remaining shareholder’s ownership by about 16.5% over the next year. Without spending a single cent, investors are effectively 'growing' their stake in PayPal's future earnings simply because the company is retiring shares at such an aggressive discount.

Risks

The main risk is that PayPal becomes a value trap. The investment case relies less on rapid growth and more on stability. If revenue and earnings decline, even a low valuation may not offer protection.

A 7–8x earnings multiple can look cheap, but declining businesses often remain cheap for long periods.

The opportunity is if the business stabilizes (or grows) rather than shrinks.

At current valuations, even modest growth or steady cash generation could justify higher prices over time.

This setup is not risk-free, but the opportunity becomes appealing if one believes stability is likely rather than decline.

Conclusion

PayPal is no longer priced as a growth company. It’s valued as a business in decline.

Yet the company remains profitable, cash-generating, and integral to global commerce. Sentiment is low, expectations are muted, and valuation reflects stagnation rather than stability.

If the business merely stabilizes, the current setup offers asymmetric risk/reward. In markets, the best opportunities often arise when a company is overlooked or dismissed.