Oil, gas, nuclear and coal are misunderstood and undervalued

What are the implications for investors?

The Contrarian Setup

Energy is one of the most hated asset classes. ESG mandates have pushed capital away from oil, gas, nuclear, and coal. Consensus expects a decrease in usage as renewables take over, though fundamentals point to rising demand.

The Thesis

Oil, gas, coal, and nuclear equities offer asymmetric risk/reward because:

Fossil Fuel usage has increased despite decades of transition spending.

Energy sources like oil, gas, and coal are more necessary than assumed, and nuclear will become increasingly critical

Power demand is accelerating from AI/data centres faster than new generation can be built

Underinvestment in nuclear across the U.S. and Europe extends the timeline over which fossil fuels remain dominant

Valuations remain depressed despite improving fundamentals

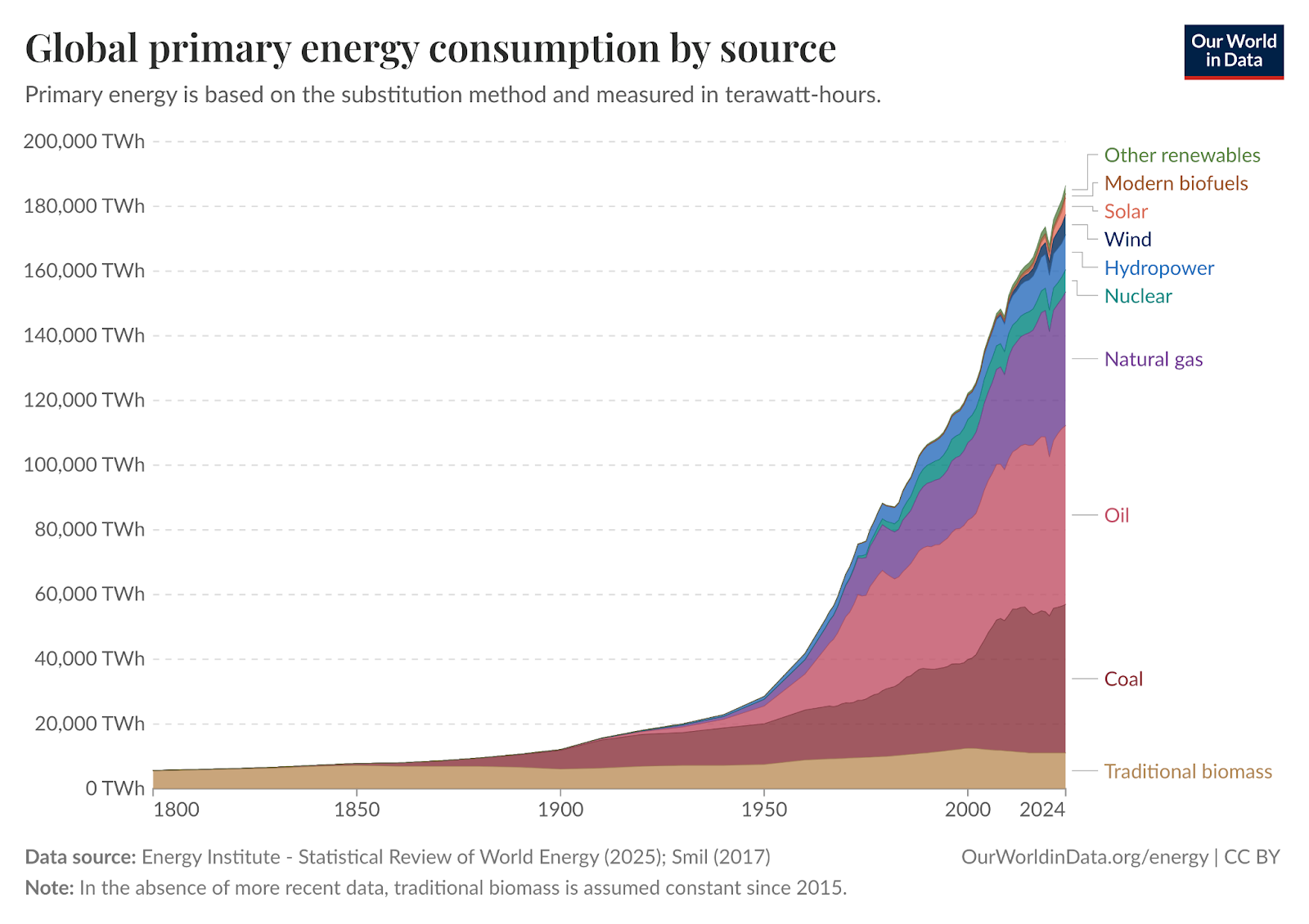

Fossil Fuel Usage Has Increased

In the last fifty years, humanity has spent six to eleven trillion dollars trying to replace fossil fuels. Most of this effort focused on wind and solar energy.

Even with this investment, fossil fuels still make up about 81 percent of global energy. This is only a slight drop from 83 percent. A two percent change in fifty years.

As money went into renewables, investment in oil, gas, and nuclear stalled. Still, demand for these energy sources kept rising.

Energy is More Necessary than Assumed

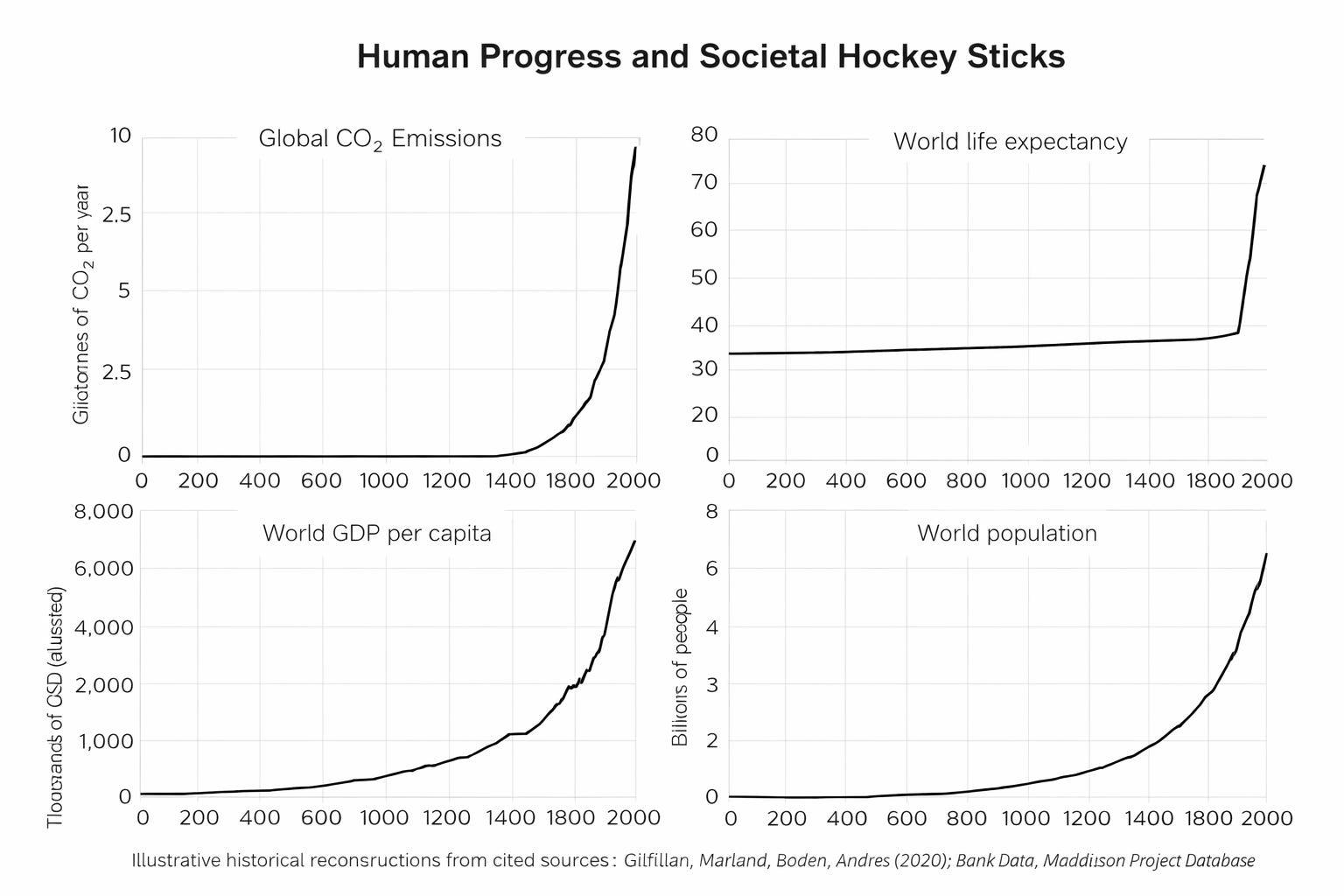

Almost everything that isn’t a rock, plant, or metal requires energy to make. Life expectancy links closely with access to energy too.

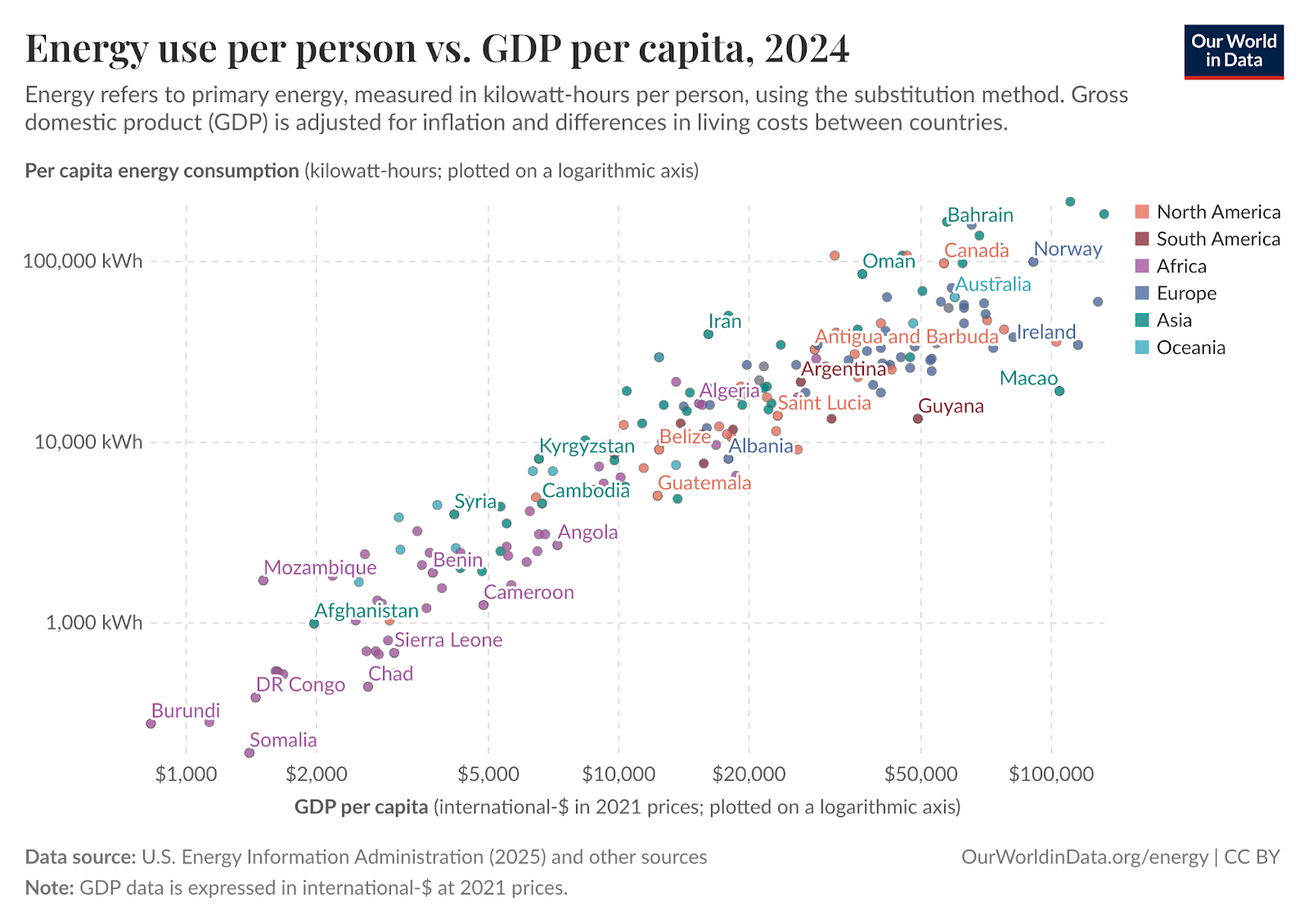

There is a clear relationship between a country’s GDP per capita and its energy usage per capita.

If billions want better lives, global energy use needs to rise, not fall.

Even the International Energy Agency, known for its early decarbonization forecasts of 2030, has adjusted its peak oil demand timeline. It now suggests demand could peak in the 2060s, reflecting the reality of rising global energy needs.

Efforts to reduce fossil fuels and CO₂ emissions with wind and solar have good intentions, but it hasn’t worked as planned. Here’s why:

Steel builds bridges, trains, hospitals, and wind turbines. Cement supports homes, roads, and water systems. Fertilizer feeds billions. Medicines require energy-heavy processes. Cities need heat, light, and functioning supply chains constantly.

Wind and solar produce power only when the sun is shining or the wind is blowing. They can’t provide power on demand for these needs.

Power Demand Is Accelerating Faster Than Supply Can Respond

At the same time, demand is accelerating.

In the U.S for example, connecting a data center to the grid takes five to seven years. On-site power can cut that time to under two years.

As a result, about one-third of planned data center capacity is now set to generate its own power. A year ago, nearly none did.

Most of these projects rely on natural gas for steady power. About seventy percent plan to use it as their main source because it’s available, dispatchable, and reliable.

However, on-site power is often less efficient and more carbon-intensive than power from a shared grid that includes nuclear, hydro, and other lower-carbon sources.

Underinvestment in Nuclear Extends Fossil Fuel Dependence

Nuclear is the only scalable, dispatchable, low-carbon power source capable of replacing fossil fuels at industrial scale. Currently, no large traditional nuclear reactors are under construction in the U.S., and new projects typically require 10–15 years from approval to operation.

Germany Case Study

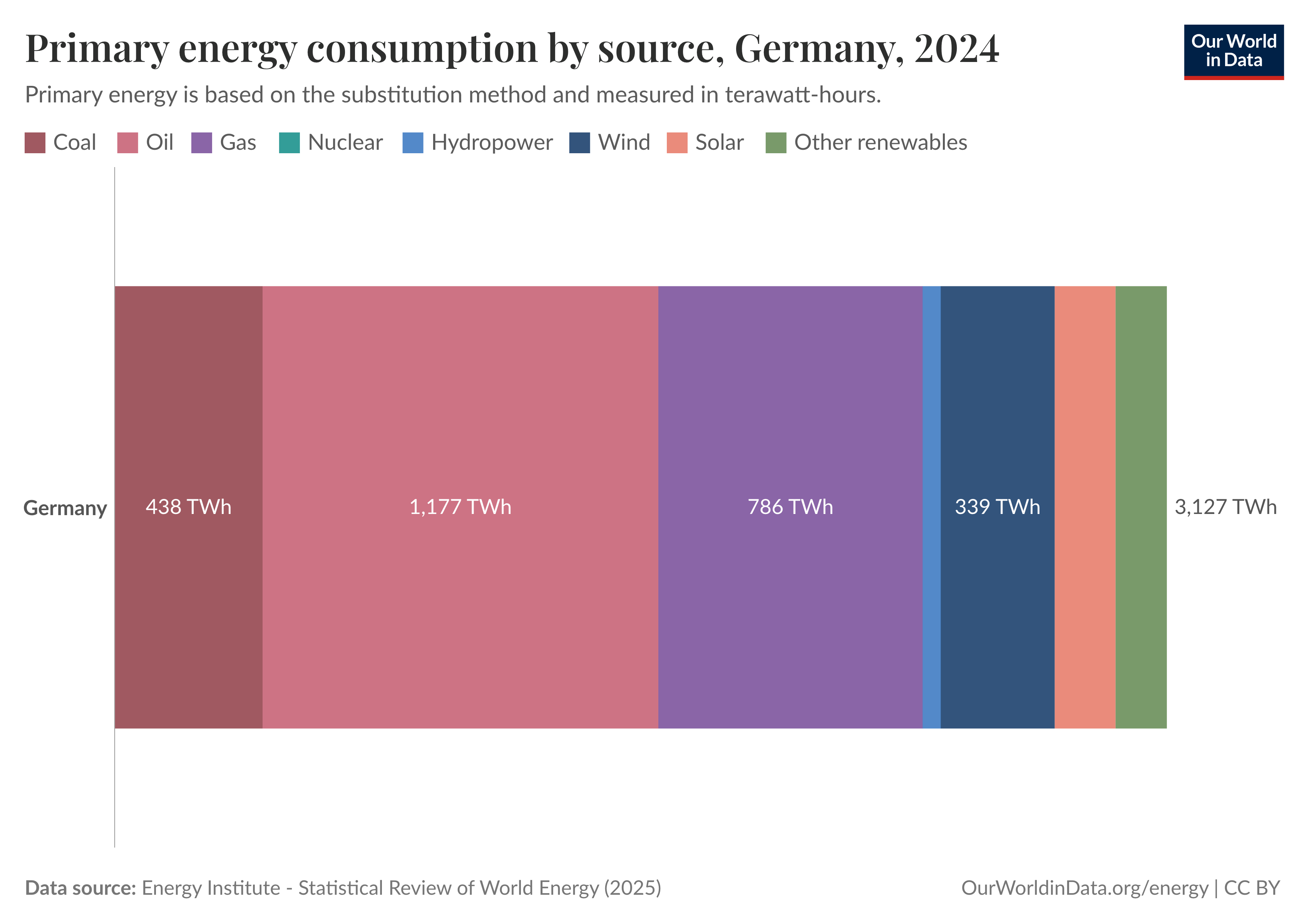

Germany shut down its nuclear plants in 2023, yet fossil fuels still make up over 75 percent of its energy use.

In 2024, oil became the largest share of primary energy consumption, followed by gas and coal. Renewables covered less than a third of total energy use.

Since eradicating nuclear, prices are now structurally higher in Germany. Estimates suggest power prices are about twenty to twenty-five percent higher than they would have been if nuclear power had remained.

The nuclear phase-out also coincided with a prolonged recession from 2023 to 2025.

In 2026, Chancellor Friedrich Merz called the nuclear exit a “serious strategic mistake,” acknowledging that reliable capacity was lost before a workable alternative was ready.

When nuclear capacity is limited before scalable alternatives are ready, fossil fuel usage extends.

What This Means for Investors

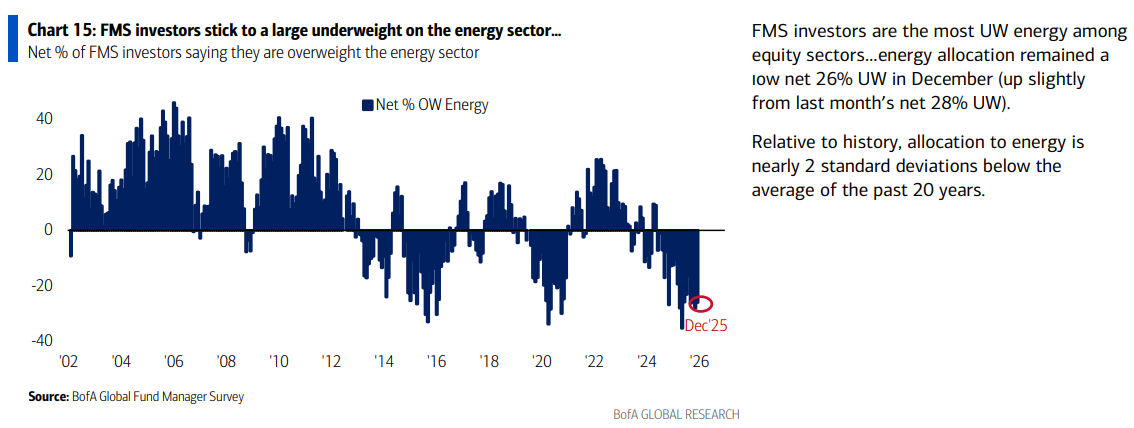

Fund managers are the most underweight energy among equity sectors. Because energy is under-owned, the tailwinds outlined earlier can lead to significant price moves.

Oil: Hated, Still Essential

Oil faces criticism, yet global demand keeps rising, creating an opportunity for investors.

Oil supports food production, agriculture, mining, construction, shipping, aviation, medical supplies, and petrochemicals. There are no scalable substitutes for many of these uses.

Industry estimates suggest oil and gas underspend by about one to two billion dollars per day while relying on infrastructure built years ago.

At around $60 per barrel, global production becomes unsustainable. This price is where new drilling, decline replacement, and future development barely meet today’s costs.

The U.S. shale industry has drilled most of its best acreage, meaning replacement barrels are now lower quality, more capital-intensive, and more price-sensitive.

Over time, costs will rise as depletion forces production into tougher reservoirs, while expenses increase due to labor, steel, services, financing, and regulations. As the cheapest barrels run out, the marginal barrel gets pricier. The longer investment remains limited, the higher prices must get to stabilize supply.

Unless a global recession or lasting geopolitical peace restores large supply volumes, oil prices must eventually rise to encourage the investment needed to maintain production.

Broad energy ETFs are starting to reflect this supply-demand imbalance, breaking through key resistance levels.

Oil services stocks, which usually lag behind oil prices, remain well below previous peaks due to a decade of capex destruction. They are also starting to break above key resistance levels.

For investors, this creates a familiar setup: an essential asset that is under-owned, unpopular, and capital-starved, yet still needed by the real economy.

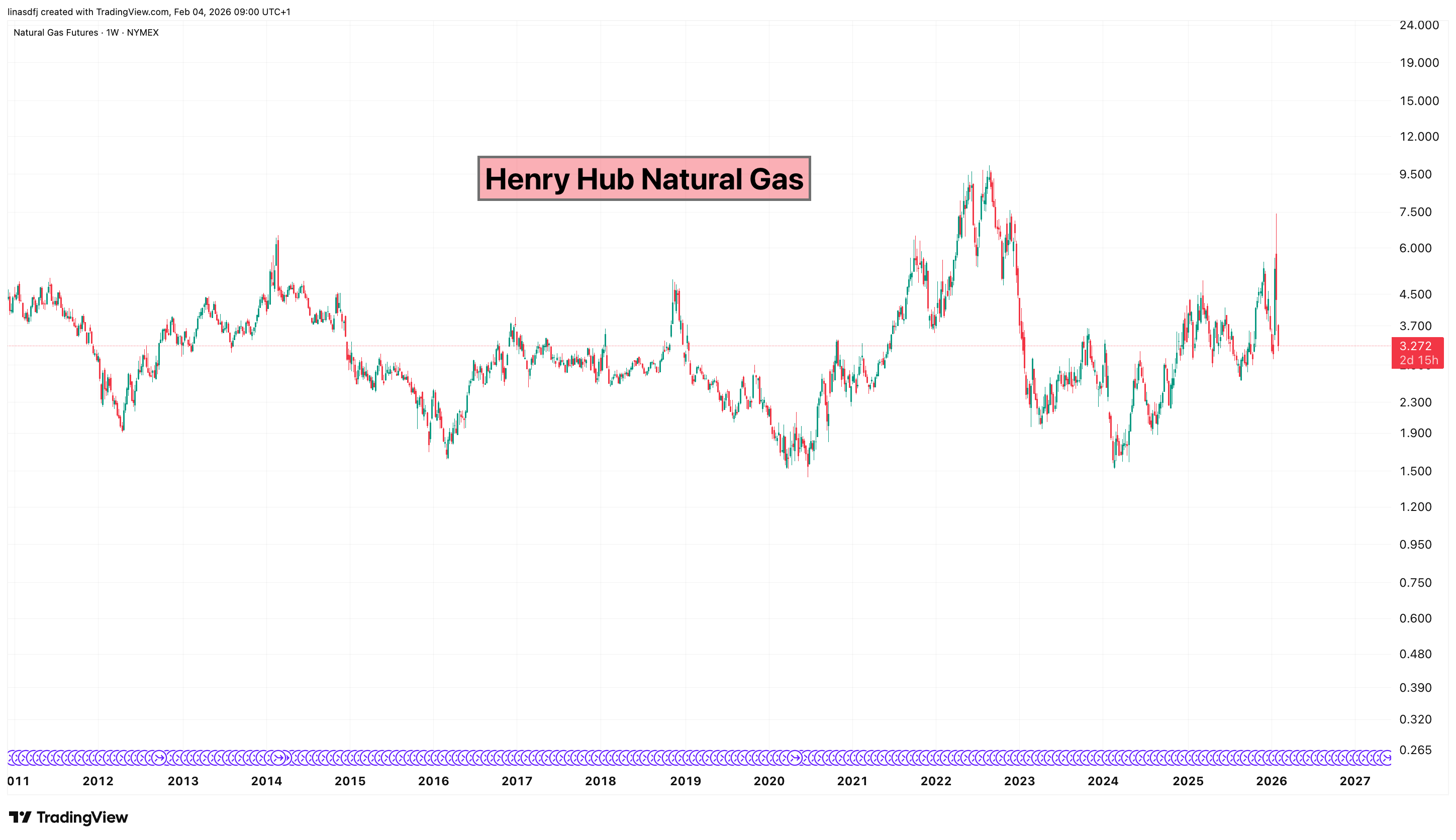

Natural Gas: The Bridge We Pretend Doesn’t Exist

Natural gas is vital for winter heating, peaking power, and keeping the grid stable when wind and solar output declines. The US benchmark for natural gas prices rose from 1.24/MMBtu to 3.2/MMBtu from 2024-2025.

Electricity demand changes by season and time of day, creating gaps that intermittent sources can’t fill. Gas covers these peaks and prevents system failures. The growth of AI infrastructure and electrification widens this gap.

Gas is also a key industrial input. It underpins nitrogen-based fertilizers and petrochemicals, essential for large-scale food production, preservation, and supply chains.

Nuclear: The Longer-Term Answer

Nuclear power is the only scalable source of clean, dispatchable energy that can meet rising demand when solar, wind or hydro, aren’t available.

It generates large amounts of electricity continuously, with near-zero operational emissions and a small physical footprint.

Unlike wind and solar, it doesn’t depend on weather and can support dense cities, heavy industry, and data-heavy economies.

However, nuclear isn’t a near-term solution. New projects require 10–15 years from approval to operation. The result is a timing mismatch: nuclear is necessary, but it cannot close today’s supply gap.

Public perception is beginning to shift. Policymakers across Europe and North America have softened prior opposition. Several countries have delayed plant closures, and small modular reactor (SMR) initiatives are gaining political backing. Technology companies have also begun exploring direct nuclear partnerships to secure long-term power supply.

Markets have noticed. The uranium complex has already repriced meaningfully higher. Vehicles such as the Sprott Physical Uranium Trust experienced significant appreciation between 2019 and 2025 as sentiment improved. Some of the biggest gains that comes from investing in deeply hated sectors has already been captured.

This timing matters for investors. Oil, natural gas, and coal benefit first because they are the only scalable sources ready to meet today’s demand. Nuclear’s opportunity unfolds over a longer horizon. As reliability becomes increasingly valuable, nuclear capacity is likely to expand, but the build timelines ensure fossil fuels remain essential in the interim.

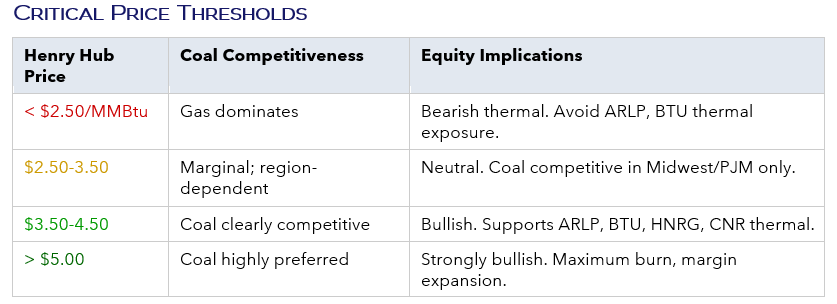

Coal: The Option Nobody Wants

Coal is perhaps the most disliked fuel in the energy system, and many investors assume its decline is permanent. In reality, coal usage has proven resilient and cyclical.

There are two distinct coal markets with different demand drivers:

Thermal coal

Thermal coal is used for electricity generation and competes directly with natural gas.

Utilities switch between the two based on economics. When natural gas is cheap, gas dominates. When gas prices rise above key cost thresholds, coal regains market share.

Metallurgical coal

Metallurgical coal is used in steelmaking and is driven by industrial demand. Roughly 70% of global steel is still produced using the blast furnace process, which requires metallurgical coal.

At industrial scale and temperature, there is no viable substitute. Each tonne of blast furnace steel requires significant volumes of coal to function.

Conclusion

Energy markets are understood by separating politics from physical reality.

Energy remains structurally under-owned in portfolios, despite being essential to the economy for the foreseeable future. Years of ESG pressure and policy uncertainty have slowed investment and limited supply growth. When ownership is this low, even small changes can lead to significant price shifts.

Sentiment reinforces this opportunity: Oil, gas, and coal are hated and often viewed as sunset industries, priced as if demand is on the verge of collapse.

Yet demand is increasing rapidly, driven by population growth, electrification, data infrastructure, and industrial activity. The gap between perception and reality is the trade here.

Timing matters.

Oil and gas are positioned for a structural bull market over the coming decade. They are the only scalable sources capable of meeting today’s demand.

Coal is different. It is not a secular growth story, but a cyclical trade. It benefits when natural gas tightens or steel production strengthens, acting as the system’s marginal stabilizer.

Nuclear represents the longer-term solution. It is structurally bullish over the coming years as reliability becomes more valuable, but parts of the uranium complex have already repriced optimism. Its timeline is measured in decades, not quarters.