The Energy Crisis Is Diffusing into Grain Markets

Overview

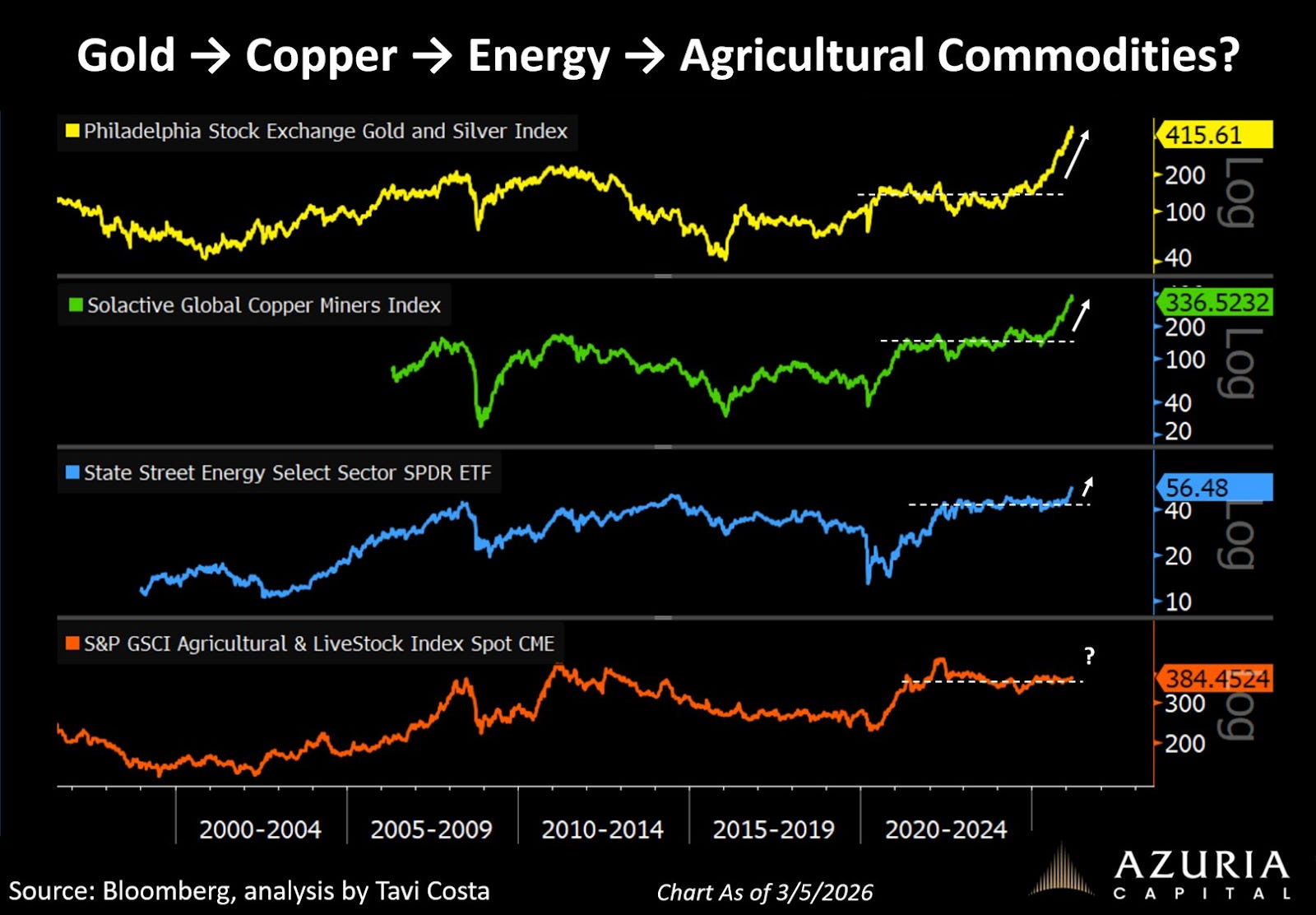

2025-2026 has been like a game of hot potato with the next commodity. We’ve rotated from precious metals, to base metals, through to energy. Agricultural commodities are next.

Each commodity will have its moment, but timing matters. Late in, you miss the move. Late out, you’re sitting through bruising drawdowns.

In this article we explore whether we’re early, the timing for a potential move, how to express the thesis, and where it could go wrong.

Context

To know where we’re going, it helps to know where we’ve been. Here are the narratives that accompanied each rotation:

Gold/Silver: The world is becoming unstable, governments are debasing currencies, sanctions are weaponising the financial system, and central banks are buying. Hold neutral money that cannot be printed.

Copper/base metals: When precious metals run, all metals tend to catch a bid. Raw materials are being consumed in the AI infrastructure buildout, and a decade of underinvestment in mining has left supply of many base metals structurally short.

Oil/Gas: ESG had starved the sector of capex for a decade. The EV transition hadn’t killed demand the way people assumed. Energy security had been chronically underpriced. Then the Strait of Hormuz closed, and oil and gas prices ran wild.

Agriculture: Next. Let’s get into it.

Agriculture Thesis

Background

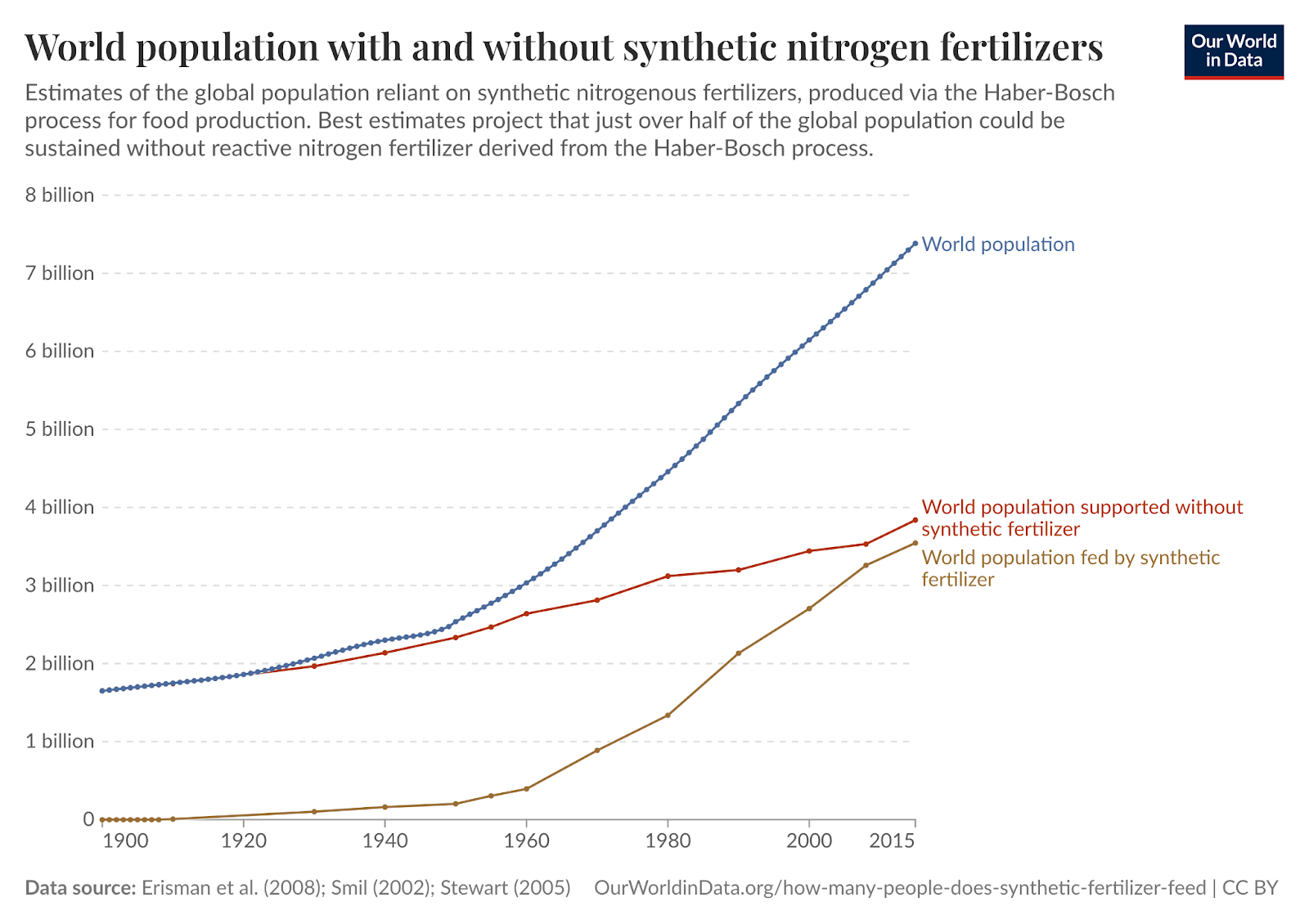

There are a number of scientific and technological innovations which have allowed for rapid growth in crop productivity. None of these had a bigger impact than the ability to produce synthetic nitrogen fertilizer. Nitrogen is the single most important input for growing the crops that feed the world.

Fundamentals

Urea

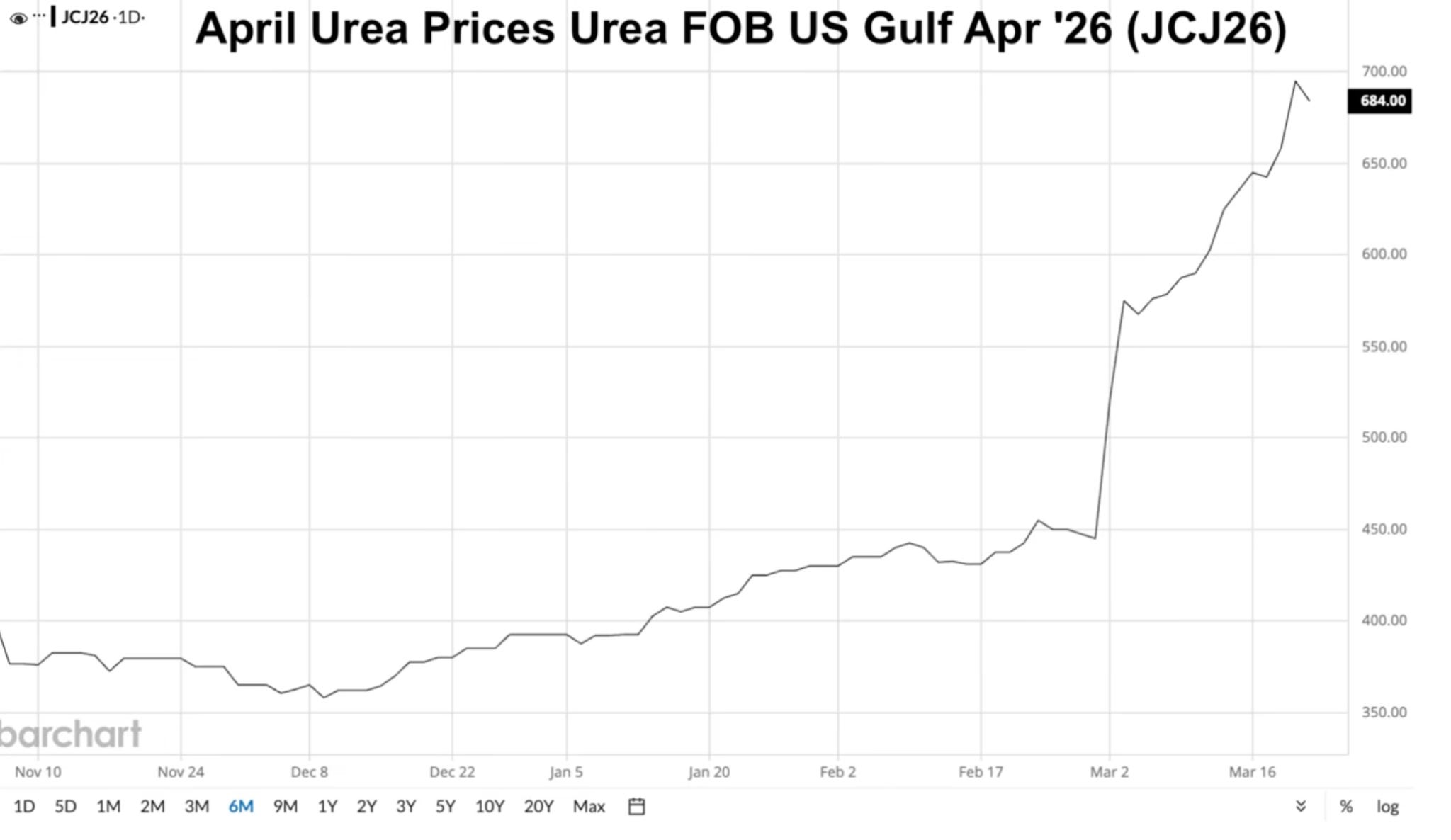

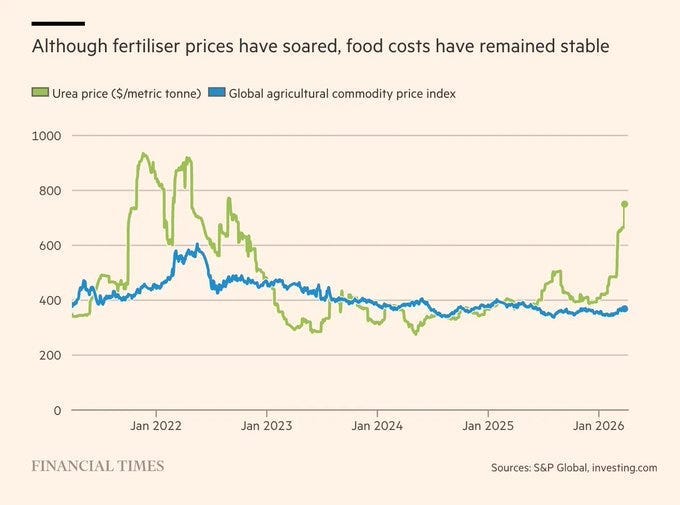

Urea is the world’s most widely produced nitrogen fertilizer. Prices have doubled since November, and with the Strait of Hormuz still closed, the direction of travel is up.

Around 1/3 of the world’s urea transits through the strait. Some countries import natural gas and produce their own urea domestically, but a similar proportion of natural gas supply is also curtailed and stuck behind the strait.

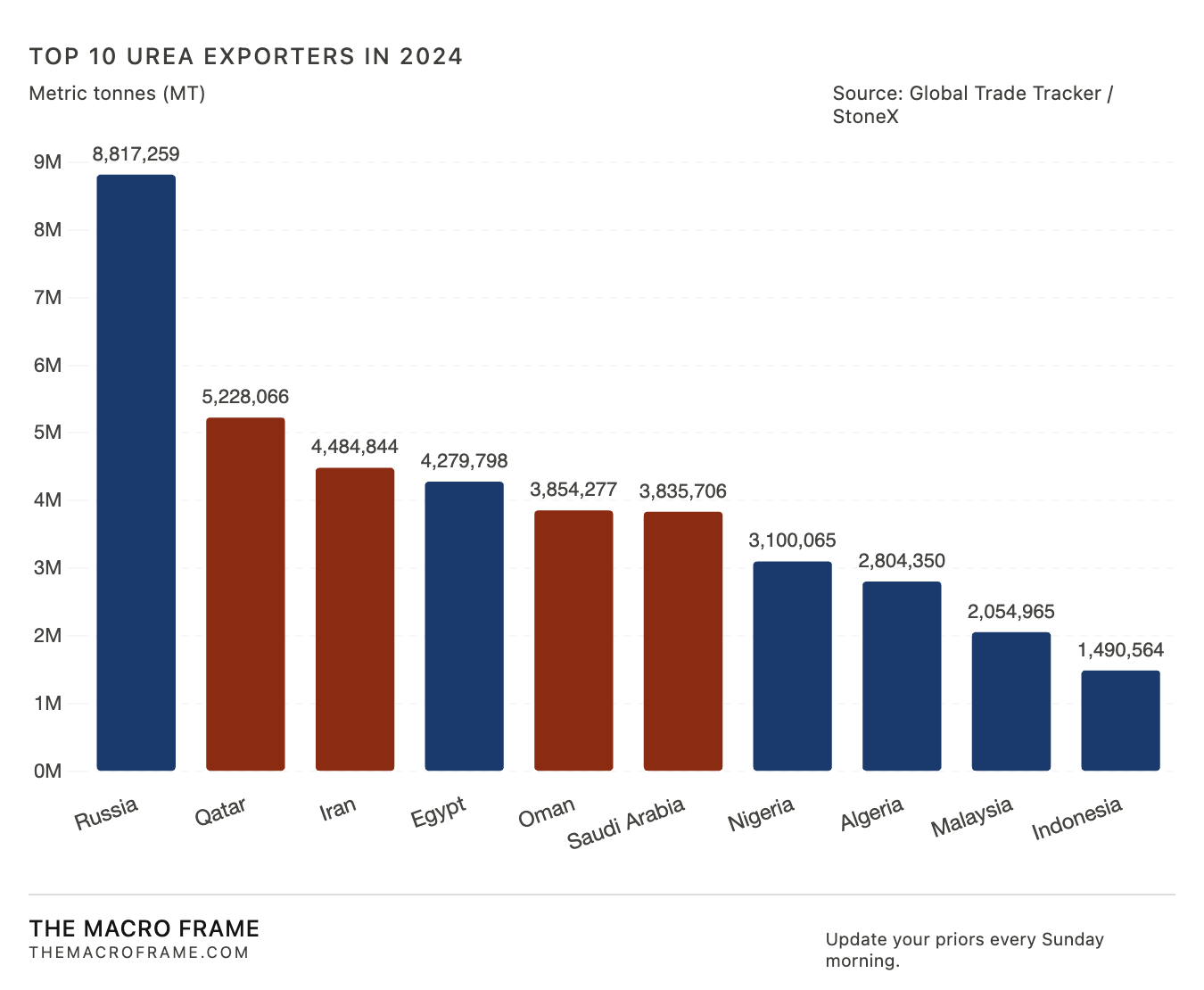

The Middle East dominates global urea supply, and right now, every major alternative source has a problem of its own:

Russia is still at war with Ukraine.

Egypt depends on Israeli natural gas, which has been cut.

Alternatives exist, but face the same constraints

UAN (liquid nitrogen fertilizer) being the main alternative, but it faces the same supply constraints.

If urea prices spike and UAN looks cheap, demand shifts to UAN and raises that price too.

Farmers are caught in a brutal cost-price squeeze

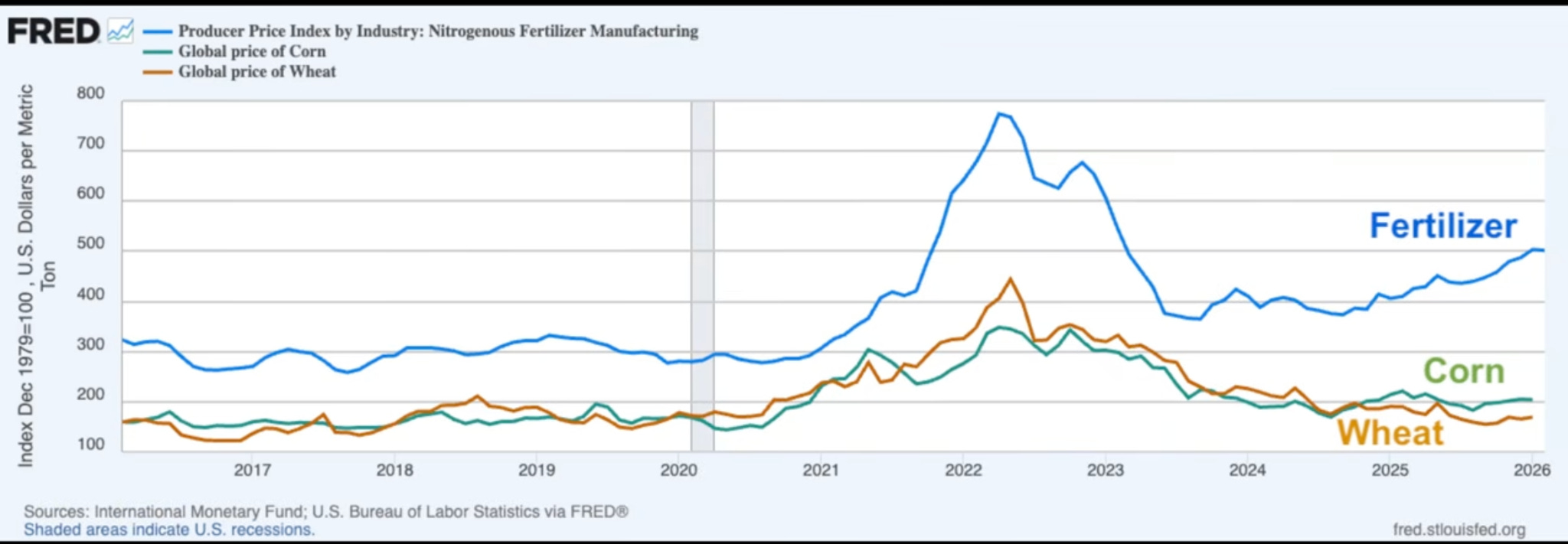

Back in 2021-22 during the start of the Russia-Ukraine conflict, the concern was losing Ukrainian wheat. Grain prices surged. Rising energy/input costs were painful, but rising crop prices provided an offset.

Today, farmers face rising input costs with no uplift in crop prices yet. It might be the most difficult cost-price squeeze the farming industry has seen. Farm bankruptcies are accelerating as the gap between production costs, seeds, fertilizer and fuel, and the market prices received for crops, corn, and wheat, has rarely been wider.

The longer this goes on, the more the supply picture shifts. Less fertiliser means fewer planted acres, which means lower yields. The market narrative moves from “we still have plenty of grain supply” to “we have lost significant yield potential and need to start pricing that in.” Other farm input costs, particularly diesel, have also risen, adding pressure to already thin margins.

Sentiment

I always like to do a gut-check on sentiment before parking money somewhere, and seeing as I don’t know any farmers personally I’m having to dig through farm-related Youtube videos to find anything of value. This Youtube channel is great, here’s one video example of many:

As one would expect, many of the comments are referencing pain, uncertainty, and the rising input costs, which is something you see nearer bottoms than tops:

Consequences for grain markets

With limited fertilizer, the question is who gets supply and at what price.

Many farmers have not yet purchased their spring fertilizer needs, and now that they are buying, the price has moved sharply against them. Some will reduce application rates. Some will plant fewer acres. Some will switch crops.

On a crop-by-crop basis, the thinking is:

Wheat is the most interesting. Most countries grow wheat, so any supply disruption travels further and faster through food systems.

Given the higher input costs, some farmers may choose to switch to soybeans, which require less nitrogen input. The market is currently pricing in a strong corn yield. If acres shift to soybeans, or yields are down, that assumption breaks.

The longer the strait remains closed, the worse the situation becomes.

The repricing window opens later this year

The repricing in grain markets is unlikely to start before mid 2026, when farmers make planting decisions and begin to assess the fertilizer price impact on the 2027 harvest.

Take a look at the 2022 increase in urea prices below. It took a few months for the increases to be reflected in commodity price index, signalling a lag between input costs, and the underlying commodity costs.

Compounding factors

Ethanol Production

When oil becomes expensive, ethanol becomes used as substitute fuel, and demand for corn and sugarcane as ethanol inputs rises alongside it. Food and fuel are now competing for the same crop.

USDA Survey

US wheat planted area has hit a century low, adding a structural supply constraint on top of the fertiliser shock. It’s just one country of many though

Weather

The corn belt is forecast to be very wet over the next few weeks, right as planting is about to begin. Below-average temperatures follow the rain, which extends the dry-off period and pushes planting dates later. Meanwhile the wheat belt is seeing little to no rain with above-average temperatures, stressing early crop development. The weather market is opening early this year, and it is not opening in farmers’ favour.

The bear case

If the strait opens tomorrow, urea prices could sell off sharply. Even so, vessels currently take around 30 days to sail to destination markets, which means supply cannot reach farmers in time for spring planting regardless.

The fertilizer supply story is now widely known and is arguably priced in. Any sign of the strait opening could trigger sell-offs.

We’re always at the mercy of the weather with yields, so a bumper crop across the biggest global producers could offset the rising input costs.

Finally, if we’re bound for a global recession, lower fuel demand means lower ethanol demand, which means lower corn demand, since a meaningful share of US corn production flows into ethanol blended at the pump.

Technicals

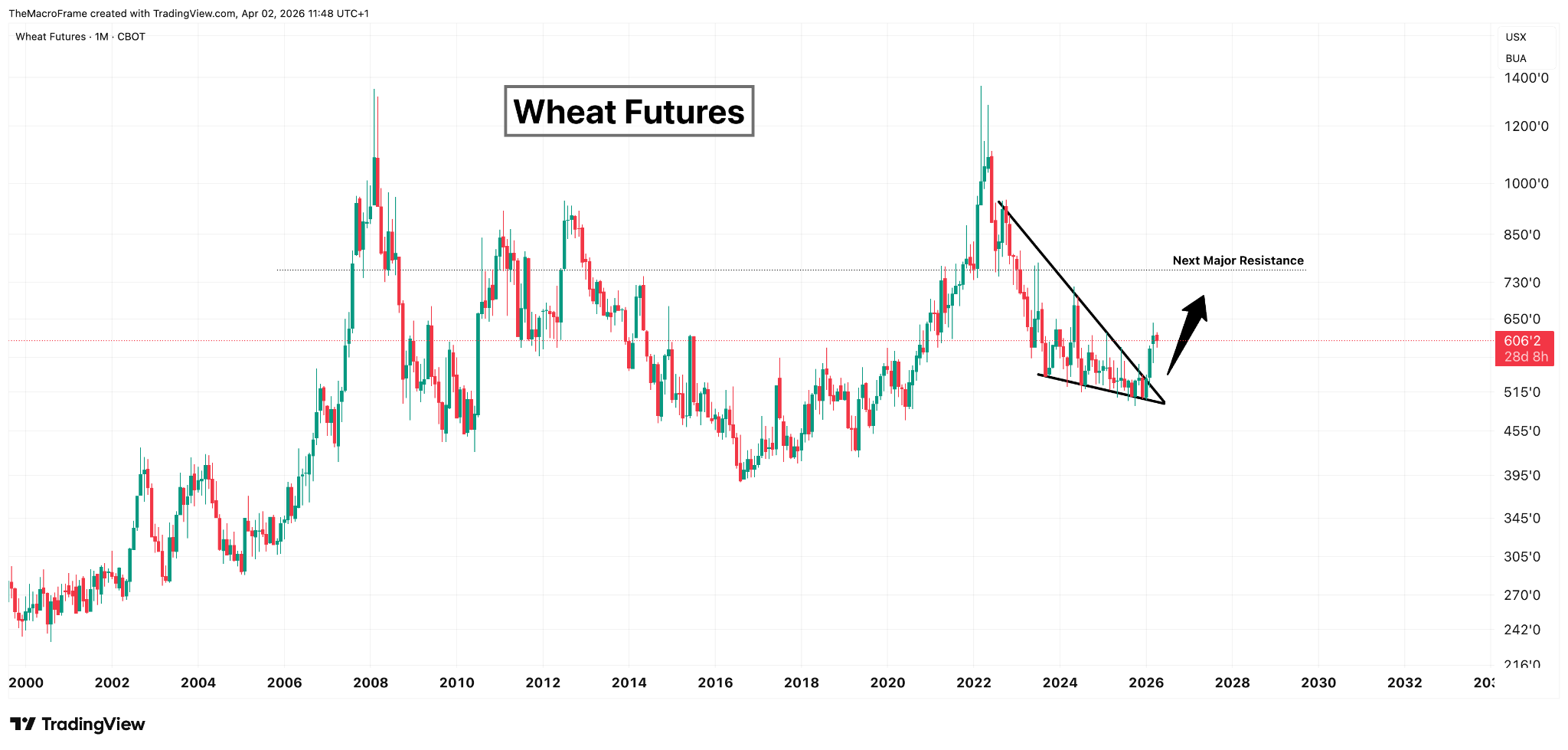

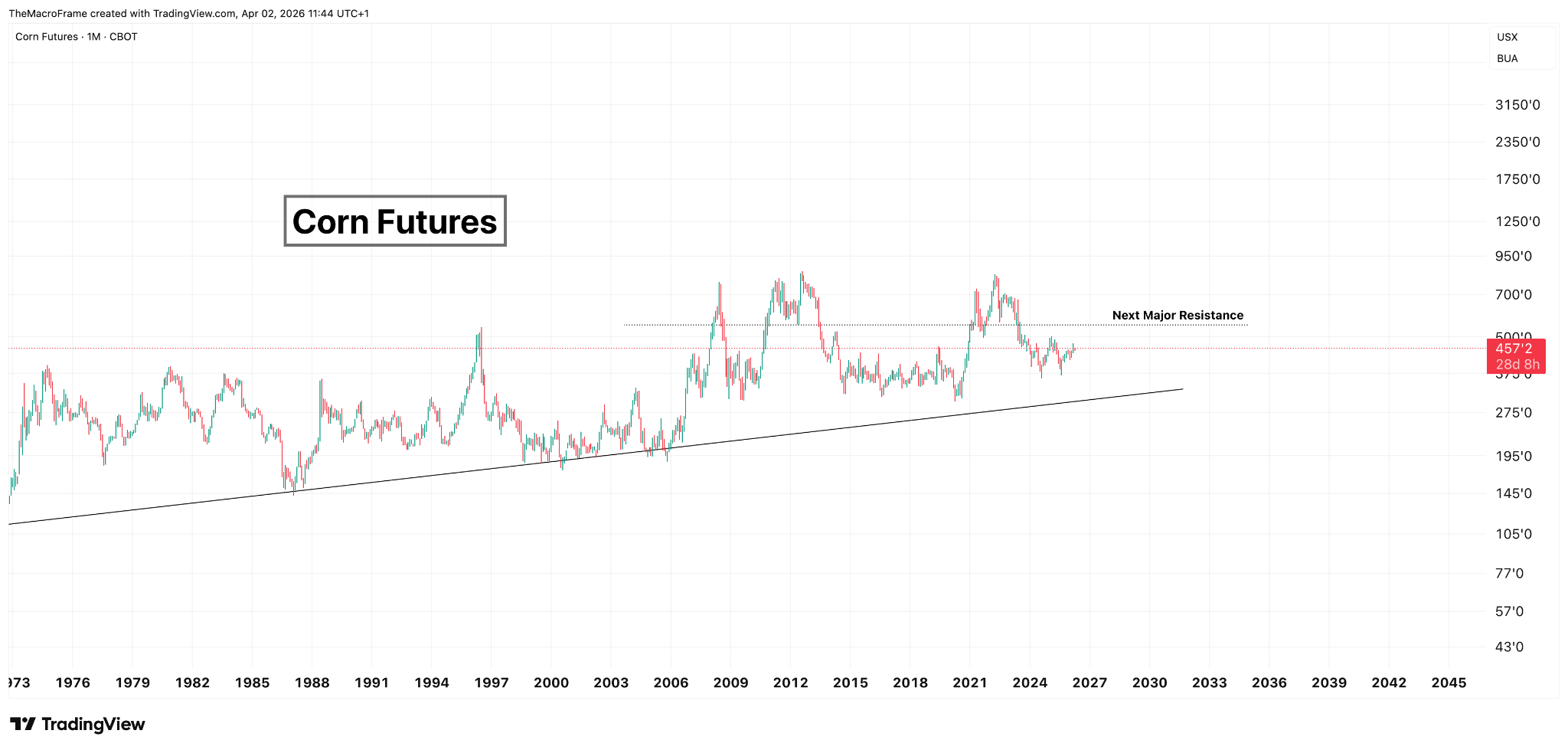

Both wheat and corn futures tell the same story from a technical perspective.

Wheat peaked near 1300 in 2022 following the Russian invasion of Ukraine, then spent the next three years in a grinding downtrend.

Price is currently sitting around 600, having recently broken out of a descending wedge formation, a pattern that typically precedes a trend reversal.

The next major resistance sits at 750. A clean break above that level opens the door back toward the 1000 range and potentially a full retest of the 2022 highs above 1300.

Corn futures are trading around 467, above a long-term upward trendline that dates back decades. The pattern is constructive. Next major resistance is around 700. Above that, the 2022 highs near 850 come back into play.

Both charts need a catalyst to break through current resistance. The fertiliser supply shock may be that catalyst.

How to express the thesis

How you access this trade depends on where you’re based.

For US investors, Teucrium offers the cleanest single-commodity exposure. WEAT tracks wheat futures and CORN tracks corn futures, both listed on the NYSE.

For European investors, WisdomTree offers UCITS-eligible ETCs for both wheat (WEAT) and corn (CORN), listed on the London Stock Exchange.

If you want broader agricultural exposure in one instrument, DBA from Invesco holds a basket that includes corn, wheat, sugar, coffee, cotton, and live cattle. You get diversification but lose the specific torque on corn and wheat that the thesis calls for.

Conclusion

The bet on corn and wheat is ultimately a bet on inflation diffusing from energy into food. It is also a bet that the Hormuz situation takes longer to resolve than the market currently expects.

The thesis breaks down in a deflationary bust. If global demand collapses, energy falls, fertiliser costs ease, and the entire chain unwinds. That is the primary risk to hold in mind.

But when input costs rise sharply and farmer margins are already negative, history suggests it finds its way into the bushel price. The lag is months, not years. The window to be early is closing.