The Problem with "VOO and Chill"

Why the Next Decade of Real S&P Returns Won't Look Like the Last

Visit any investing forum these days and you’ll hear the same advice on a loop: “Just VOO and chill”, which is internet meme-speak for “Just buy the S&P 500 to the total exclusion of individual stocks or other asset classes”.

Every social media platform is bursting with market participants piling into low-cost index funds, like VOO 0.00%↑, with every paycheck, come rain or shine. If you ask them why they adopted this strategy, they point to two stats:

The 10-Year CAGR: An outstanding annual return of 13.65%.

The Active Failure Rate: Around 85% of actively managed funds fail to beat the S&P 500 over a 5-year period.

These are genuinely impressive stats. But there are lesser-known tectonic macro shifts that make the next decade of S&P only investing likely less impressive than the last.

That’s not to say to ditch the S&P entirely… For many investors, having an allocation to the S&P makes perfect sense. But the all-in index strategy should be re-considered and I suggest some minor portfolio changes one could make to weather an upcoming S&P storm.

Brief History of the S&P 500

In 1975, Jack Bogle founded Vanguard, and the next year, he introduced the first index fund for individual investors. This fund tracked the S&P 500, which follows the top 500 US companies, weighted by their size.

Because the fund is market-cap weighted, when you invest, your money automatically flows most into the largest companies.

In 2026, index-investing is the norm. Some people put money in deliberately every month, adopting “VOO and chill” as a strict rule and not trying to time the market highs and lows. Others invest this way by accident through automatic enrolment in workplace pensions.

In both cases, money flows in without considering valuation. “Did you give me cash? Then buy.”

The Problems with “VOO and Chill”

1. Overvaluation Risk

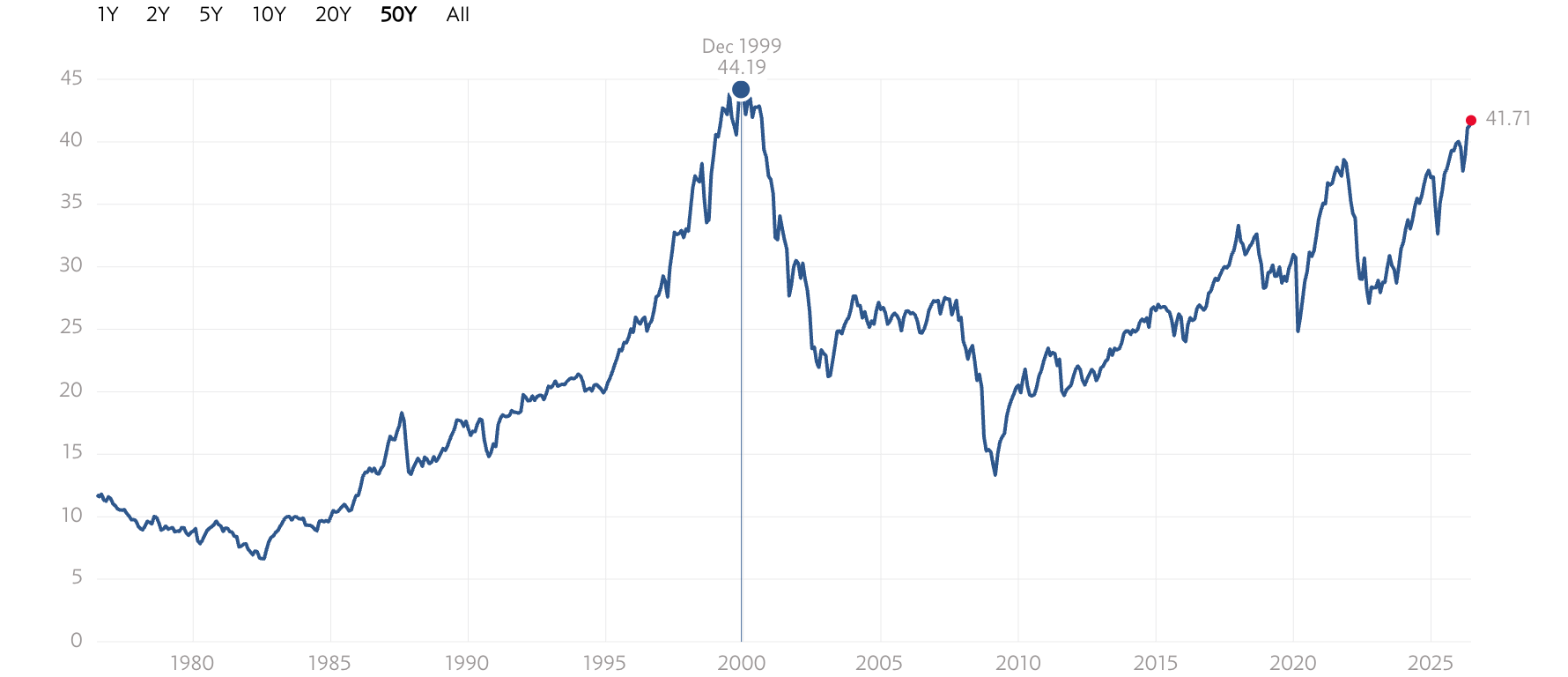

Dr. Robert Shiller, an economics professor and Nobel laureate at Yale, two decades ago introduced the Cyclically-Adjusted Price-to-Earnings (CAPE) ratio, also known as the Shiller P/E ratio. CAPE compares the S&P 500’s current price to its average inflation-adjusted earnings over the last decade.

The CAPE ratio currently sits around 41, compared to a historical median of ~16. The only other time U.S. valuations reached this extreme was during the peak of the dot-com bubble.

When you graph the CAPE on one axis and inflation-adjusted returns on the other axis, you get an inverse correlation. A higher CAPE starts decreasing the odds that investment returns will be decent over the next 15 years:

2. The End of a 40-Year Tailwind

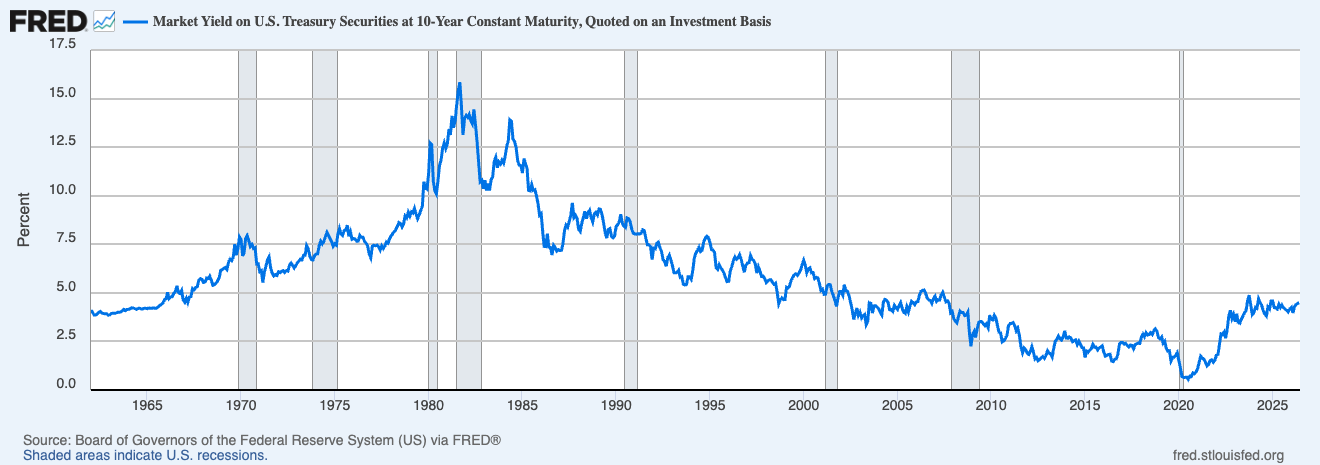

The 10-year Treasury yield affects many things, including mortgages and corporate debt. It was around 15% in 1981 and dropped to almost zero by 2020.

This decline over four decades was a big part of the success of the index funds and US equities in general. When rates fall, stock valuations rise because future profits become much more valuable today.

By 2020, rates had hit their lowest point, and that forty-year trend ended.

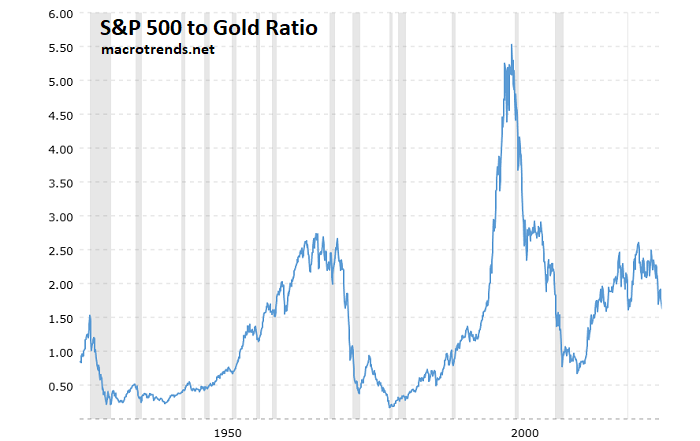

Although US stocks have gone up in dollar value since 2020, they’ve dropped when priced in gold, which highlights another issue — dollar debasement. Assets, like the S&P 500 have charted higher in $$ terms, while in a bear market against other assets like gold.

3. Sentiment Is Stretched to Extremes

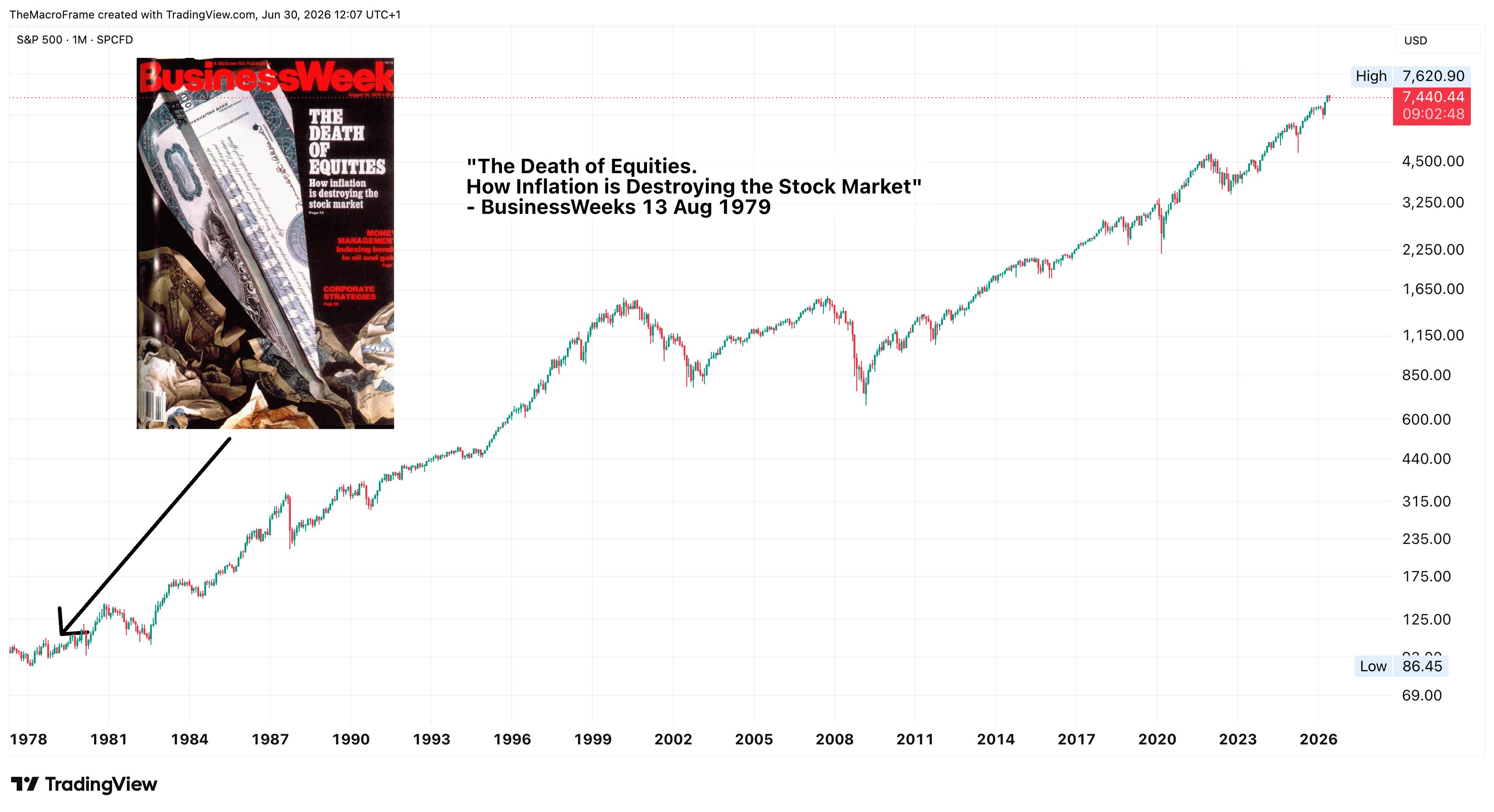

In 1976, at their inception, market-cap weighted index funds faced harsh criticism; detractors called them “un-American” and “a path to mediocrity.” This mirrored a general disdain for stocks, highlighted by BusinessWeek’s infamous 1979 cover declaring the “Death of Equities.”

That cover ultimately signalled a generational bottom for stocks. Skeptics gradually turned into buyers, fuelling a decades-long boom, with intermissions.

Today, sentiment has inverted: stocks are seen as a safe haven. Thousands of books promote “VOO and chill”- type investing frameworks. Influencers hammer this home to their audiences daily. Threads on r/investing are littered with phrases like “VOO and chill, time in the market, just buy the index.”

What once labelled you a fool is now universal wisdom. Just as overly negative sentiment marked the start of a major uptrend, overly positive sentiment often marks the top (in real, inflation-adjusted terms).

4. Concentration and Geopolitical Risk

While the U.S. still enjoys the largest capital markets in the world, trust in the U.S. as an economic safe haven is being tested.

Sanctions, Tariffs, Greenland threats, concerns over the global power and reach of U.S. tech companies, all impact the perception of the U.S and are contributing to straining relations with allies:

One in three German consumers now refuses to buy US products outright. In Austria, 71% say they’re prepared to boycott. In Sweden, the figure is 70%. There is not a single country in Europe where more than half the population holds a positive view of the US.

If you live in Europe, you’ll have noticed a trend. EU companies are leaning into their origins as a selling point. Bolt, the European rival to Uber, now stamps “Made in Europe” on its welcome screen.

Time will tell whether this trend is durable, and to what extent it hits US capital markets and equity valuations. But it feels more lasting than the typical boycott.

5. Demographics: The Changing of the Guard

During the historic bull run, Baby Boomers were in their peak earning years, providing a steady stream of market demand via payroll deductions.

Now, Boomers are retiring rapidly and shifting from net buyers to net sellers to fund their retirements.

Furthermore, the incoming generation views investing through a different lens: According to Bank of America’s 2026 Study of Wealthy Americans, younger investors put only 32% of their portfolios in stocks, compared to 58% for boomers, with the rest going into crypto, gold, and other alternatives.

6. Institutional Fragmentation

The long S&P 500 bull market developed within an era of a more unified institutional narrative. Today, trust in legacy institutions and media has fallen precipitously.

The way we invest is fracturing alongside it. While passive investing still supports traditional indices, a growing share of capital is opting out entirely, flowing into assets like Bitcoin and gold that sit outside the conventional equity system and carry no counterparty risk. If pension providers eventually offer automatic enrolment into these assets, the steady demand underpinning stretched index valuations will face real pressure.

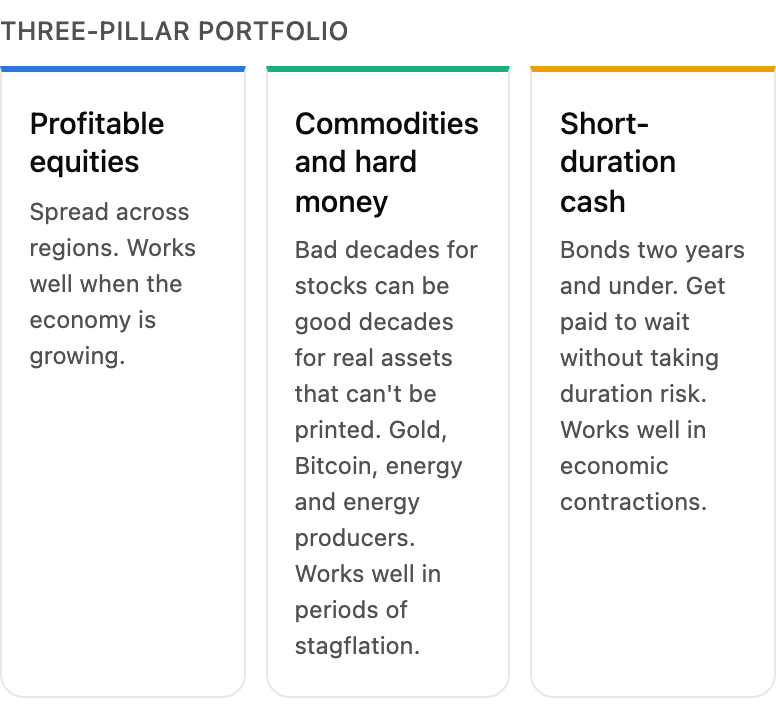

How I am Mitigating These Risks

Given the problems outlined above, I am building what I think of as a three-pillar portfolio, similar to the framework Lyn Alden recommends here:

Profitable equities, distributed by region. In a multi-polar world where trust in the US is eroding, I spread risk across multiple countries rather than clustering all my capital in a single US index. Profitable is the key word. I avoid the unprofitable growth names that passive indexes force you to own.

Commodities and hard money. Bad decades for stocks tend to be good decades for other assets. The 1970s were terrible for equities but excellent for commodities and hard money. I hold an allocation to commodities and commodity producers, including uranium and oil and gas producers. I also hold gold and Bitcoin, the hard-money pillar the S&P and bonds have no answer for.

Cash and short-duration bonds. Be prepared for drawdowns of 30% or more that span multiple years. I hold a buffer in cash and short-duration government bonds, so I have some dry powder without taking duration risk.

Final Words

While index funds have been a great strategy for many people, cracks are appearing, alongside record valuations and stretched sentiment.

Investors don't have to be all-in on the S&P 500. Active portfolio management doesn't have to mean finding the next Nvidia and hoping for a ten-bagger.

There is a happy medium where we pay more attention to the shifting world and make small, rational adjustments to our portfolios to accommodate it.

This is not a call for a crash in the S&P 500. It is a call for lacklustre real returns over the next 1-2 decades.

For the next year or two, my thesis will look premature. Good. These pieces should feel uncomfortable at the time of publication. They take time to prove out. The diehards will spend years mistaking the final gasps of the old “Voo and chill” regime for continued validation. By the time they adjust, it will be too late.