Why Everything Made of Metal Is Going Up

What the metals rally reveals about human behaviour, money, geopolitics, and supply

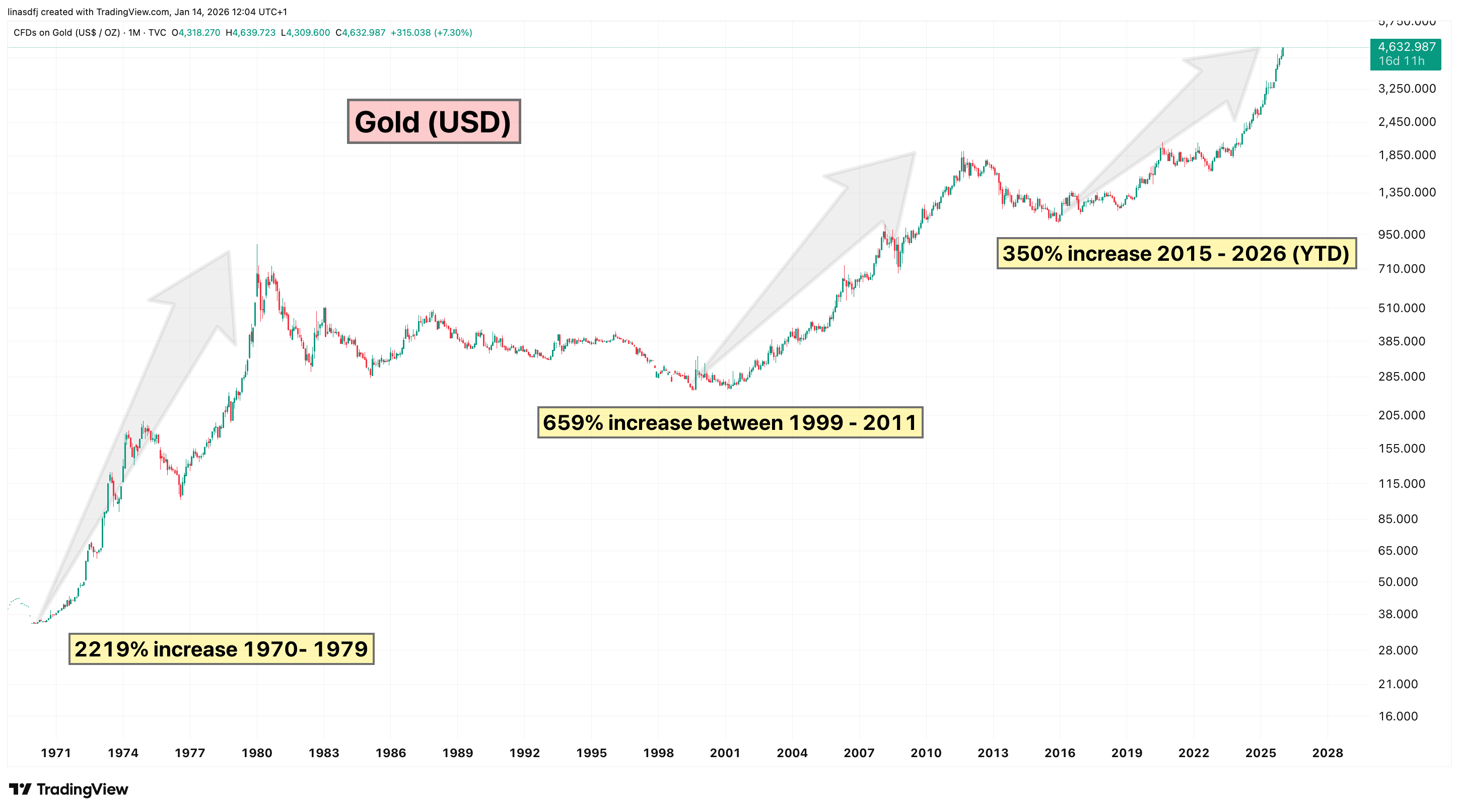

Gold has surged through 2025. Silver is up 6x since the COVID panic. Platinum and palladium are breaking out. Rhodium has doubled. Copper and aluminium are up too.

Everywhere you look, something made of metal is moving.

This isn’t a fad either. Since the turn of the millennium, gold has materially outperformed the S&P 500. A “pet rock” has beaten the world’s most celebrated equity index.

So what’s going on? What’s pushing metals higher, what does this tell us about investor behaviour, and can history help frame how far this move can run?

The background conditions behind the move

Ownership: empty space above the price

Metals remain marginal in most portfolios. The ETF data makes this clear: gold’s share of total ETF assets is still near cycle lows and far below prior peaks.

What about retirement capital? NEST, the UK’s largest auto-enrolment pension scheme with over 13 million members. In its default Retirement Date Funds, you will find global equities, bonds, and property. What you will not find is a dedicated allocation to metals. No gold exposure. No mining allocation.

Take sovereign wealth funds. The Norway Government Pension Fund Global, one of the largest pools of capital, has a ~3% allocation to gold and metals miners.

Look across institutions and the picture is consistent. Most large portfolios run zero to low single-digit exposure to metals. Where commodities exposure exists, energy tends to dominate and what remains for metals is slim.

Because metals are structurally under-owned, catalysts create parabolic moves.

Sentiment: Disbelief as fuel

A few years ago, metals were subject to ridicule.

Gold was for doomers and owning metal marked you out as someone who had given up on the system.

This kind of sentiment is important because it creates room for price to run. When an asset is widely dismissed, the sceptics can become future buyers if conditions change.

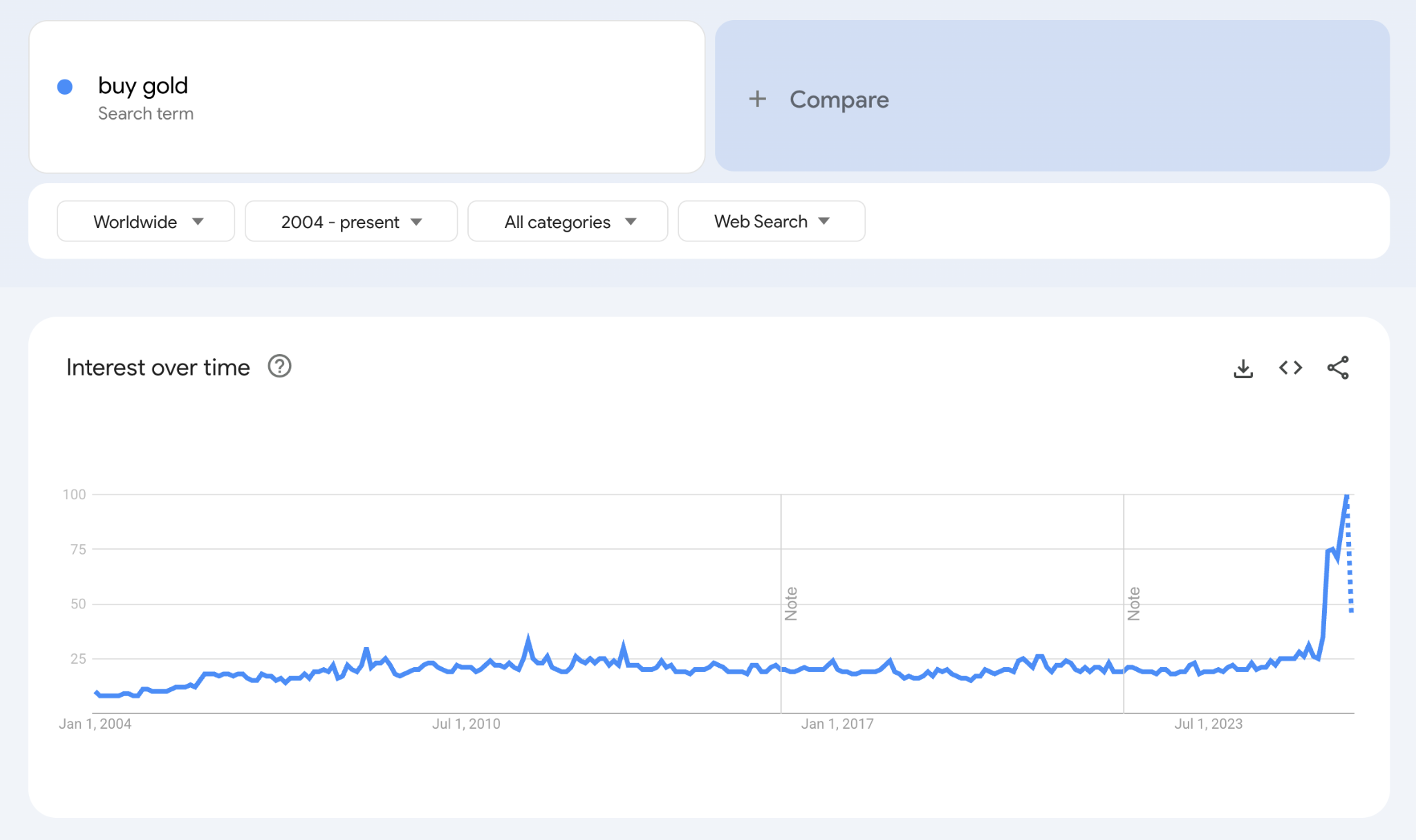

Well, as of the middle of 2025, those conditions are changing. Google Trends shows a rise in searches for “Buy Gold,” suggesting broader awareness is building.

Anecdotally, I’m seeing changes on the ground too. Here in Portugal, signs offering to buy and sell gold have started appearing in public places. A late-cycle signal that appeared in previous gold bull markets.

In October 2025, reports described thousands queuing daily in Sydney to buy gold. Many buyers were there simply because they had read about gold in the news.

Google Trends, sign-posts, and queues are treated as unsophisticated signals, but they’re informative when layered. History suggests that they appear later in a move.

Catalysts

We’ve discussed the background conditions that create room for prices to move. But conditions alone don’t drive sustained rallies. What turns a setup into action is a catalyst colliding with real supply and demand constraints. That’s where we turn next.

Weaponisation of Money: The Spark

Ownership and shifting sentiment create the space and fuel for a rally. What turns that setup into price action is a catalyst, alongside supply and demand.

Over the past few years, money has become a weapon of war.

The invasion of Ukraine was the most obvious example of this. Sanctions were rolled out at speed: Russian assets were frozen and banks were cut off. At the time, many celebrated what looked like the instant destruction of the Russian economy.

The second- and third-order effects were not discussed.

When countries use sanctions, they make access to the system conditional. They’re saying “your money works only as long as you follow our rules”.

Countries that fear being sanctioned do not want their savings sitting inside someone else’s system with fluctuating rules. They start looking for places that sit outside the system.

We see this on smaller scales too: Individuals are de-banked for not following the rules of the system are forced to rely on money that sits beyond reach, whether that is physical cash, gold, or bitcoin.

At the state level, the response has been clear: Russia increased its gold holdings under sanctions pressure. Other countries followed.

When money becomes conditional, neutrality matters. Metals are neutral.

Debasement: The pressure cooker

Governments fund themselves by printing money.

Of course, they don’t tell you that! They call it stimulus, easing, or something like that. While the names may differ, the result is the same: Over time, dollar, euro, pound, or yen that you hold in your wallet buys less than it used to.

This is obvious, you see it over time when visiting the shops: The price of goods and services rises year after year.

That pressure doesn’t stop at groceries either. It applies to everything priced in currency. Yes, including metals.

For decades, bonds were supposed to protect you from this, but they don’t anymore. Yes, you earn interest holding government debt, but you’re being paid back in lower value currency units and over time your purchasing power is going down.

This is where metals fit. Unlike fiat currency, they are:

Not printable

Not dependent on policy credibility

No one else’s liability

Not cancellable

As long as currencies are being debased - a structural feature of how governments fund themselves - scarce assets with real-world demand tend to exert a gravitational pull higher over time.

Demand Accelerator: The AI trade is a metals trade

Most people are long the Mag Seven, whether they know it or not. Passive money flows through index funds, pensions, and savings plans.

What very few people are long is what those companies are buying.

The AI trade is often framed as a software or subscription story. In reality, it is increasingly a physical one. The largest technology firms are converting financial assets into infrastructure: data centres, power generation, cooling systems, and hardware.

That infrastructure is metal-intensive:

Copper (power, wiring, transformers)

Aluminium (cooling, structures)

Silver (conductivity)

Uranium (grid stress, baseload power)

Steel and specialty metals

AI is a powerful source of demand, but it is not the only one.

These same metals are also critical inputs for energy infrastructure, electrification, defence, transport, and industrial manufacturing.

In other words, AI adds pressure to markets that were already tight.

Price-inelastic supply: the absence of a brake

In many markets, the cure for high prices is high prices. Rising prices attract supply, and supply eventually cools the move.

Across the metals complex, supply is constrained by geology, bureaucracy, and time. New supply can take years to arrive, regardless of price.

Copper is a good example. From discovery to first production, a new copper mine typically takes 10–20 years.

Other metals show rigidity too:

Silver: ~70% of global silver supply is produced as a by-product of copper, lead, zinc, or gold. You don’t mine more silver unless you mine more of something else.

Platinum group metals: ~75% of global platinum supply comes from South Africa. Production is concentrated in a handful labour-intensive mines with high political and operational risk.

Nickel: Around 40% of global supply now comes from Indonesia, much of it policy-dependent and tied to laterite processing that is capital-intensive and environmentally constrained.

Tin: Supply is extremely concentrated. Roughly 50% of global output comes from just three countries. A single mine in the DRC accounts for a high single-digit percentage of world supply.

Aluminium: Over 60% of production costs are electricity. Smelting capacity depends on cheap, stable power and multi-year buildouts.

Gold: Average ore grades have been declining for decades. Higher prices often offset rising costs rather than unlock meaningful new volume.

When demand begins to hit this scarcity, and the conditions outlined above are in place, prices tend to move sharply higher.

Where Are We in the Cycle?

Structurally, the forces pushing metals higher have not gone away:

Supply and demand imbalances remain

Physical constraints are still real

Debasement remains a feature of the system

Geopolitics continues to push capital toward neutral, hard assets

What has changed is positioning and mood. Ownership is beginning to rise from very low levels, and sentiment has shifted from ridicule to curiosity, and now toward optimism. As that transition unfolds, the easy upside has gone.

This is what mid-cycle excess tends to look like.

In past metals bull markets, the strongest advances were interrupted by sharp 30–40% pullbacks. They reset ownership and sentiment, which created the conditions for the next leg higher.

That is where we likely are now: not at the end, but no longer early either.

Conclusion

The metals complex looks tactically overvalued, given the magnitude of the recent moves, sentiment turning optimistic, and ownership increasing. The metal markets look ripe for a correction, even while the structural trend remains bullish.

A reminder that pullbacks in the last metals bull market were deep and often ran for multiple years.

While the market appears tactically stretched, over the next decade the conditions that have driven the bull run so far show no signs of slowing:

Money will continue to be debased

Debt will keep growing

Money will continue to be weaponised as a policy tool

Supply and demand constraints will matter

Neutral, non-liability assets will retain a role in portfolios

That alone does not guarantee prices move steadily higher. If history is any guide, this cycle will include gut-wrenching 30–40% drawdowns. We haven’t had those yet.

Are you ready? Are you sure?

Structurally, the case remains in place for the next decade.